Last week, the Federal Reserve Bank of Minneapolis released a new report analyzing St. Paul’s housing trends and outcomes. It comes to the conclusion that the city’s policy landscape is a mixed bag. Attempts to reduce rent increases may have had unintended consequences, dampening new construction, whereas loosening restrictive zoning regulations seems to have helped.

My first reaction: I’m glad someone more accomplished than me is tracking housing trends in St. Paul. Back in 2021, as debate raged over the city’s referendum on strict rent control, it felt like I was the only one cobbling together housing statistics. For months, I’d spent hours on a spreadsheet tracking years worth of monthly Department of Housing and Urban Development data, hoping to understand how the city’s changing housing policies were impacting supply.

Related: How Minnesota lawmakers defied expectations to pass a bipartisan affordable housing law in the session’s final week

Thankfully, a lot has changed. Two years ago, the city of St. Paul began publishing housing data on a dashboard, even breaking down housing construction by geography and subsidy status. The website is refreshingly complicated, showing how different data methodologies portray different trends.

Then last week, the Minneapolis Fed team weighed in with its own St. Paul housing dashboard, alongside a slim-yet-punchy summary. The report lays out the city’s roller coaster policy landscape and its effects on construction and tax base, while offering comparisons with similar urban markets. The main takeaways are that St. Paul’s policies have had conflicting effects on its housing supply, its tax base is suffering, and despite increasing affordability problems, rents have stayed pretty much flat.

Countervailing forces on new construction

Those with longer memories will recall the 2021 rent control referendum, and how the public argument centered on the effect the new referendum might have on housing supply and affordability. As predicted, rent stabilization policies and politics in both St. Paul and Minneapolis have dramatically reduced new housing construction.

Because of that impact, St. Paul officials amended the city’s rent stabilization policy more than once since the original strict approach was approved by voters in 2021. (See my articles on this: the first policy, the second policy and the in-place third policy.)

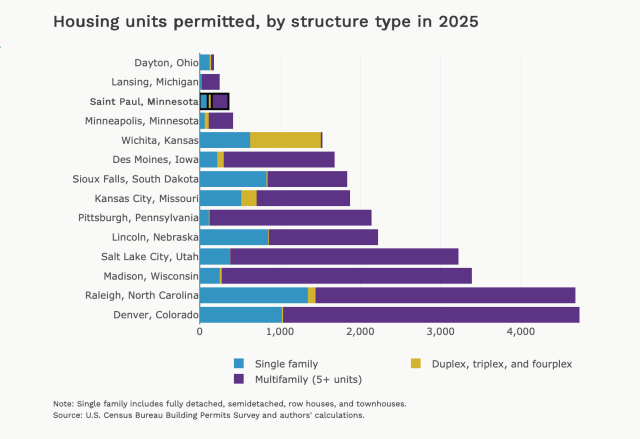

It turns out that, amid the chaos, St Paul’s housing production has dropped precipitously and, it’s worth noting, so has the Minneapolis trend line. As the Fed report points out, the numbers are so bad that St. Paul saw fewer apartments built last year than Lansing, Michigan, a city that’s been shrinking for a half-century.

Drawing on interviews, the Fed researchers point to the effects of rent stabilization politics on investment, specifically access to financing for housing developers. There’s no economic or geographic reason why Madison, Wisconsin; Wichita, Kansas; Lincoln, Nebraska; or Sioux Falls, South Dakota, should each be building twice as much housing as Minneapolis and St. Paul combined. The Twin Cities has a strong economy, at least when masked ICE agents aren’t on the streets.

At the same time, zoning reforms have made it easier to build new homes, providing a “carrot-and-stick” policy approach that’s hard to scrutinize. Developers will have to be creative about lining up financing for Twin Cities projects, as a percentage of investors will likely remain unwilling to finance local projects for a long time to come. (See this example of a new development under construction on Grand Avenue.)

Feedback on St. Paul implementation

Another key finding of the Fed report is that the evolving implementation of the rent stabilization law has not been as effective for landlords as policymakers would have liked.

Here’s a key quote:

“Owners of rental housing expressed frustration about this process. One noted that their financial challenges ‘would need to be catastrophic before going to the rent control board’ because they don’t want to make their operating costs public. Another owner shared frustration about the city’s relative lack of capacity — both in number of staff and their real estate experience — in reviewing exemption requests.”

Not wanting to reveal one’s expenses is certainly suspicious, and that complaint seems like a self-created problem for building owners. But it’s also a sign that the regulatory process does not seem to be working as designed.

If landlords are overwhelmingly ignoring both the city’s vacancy decontrol and “reasonable return” provisions, avoiding any adjudicated process altogether, it seems like many apartment owners are simply raising rents 3% per year, to the extent that the market will bear it. That’s not a great outcome for renters.

Related: Federal Reserve report identifies challenges for developers and renters alike in Greater Minnesota

Another side effect is a depression of apartment values, another mixed bag for the city. On one hand, if real estate values in St. Paul are low, rents will also be low. The study points out that rents are flat on average, even if this calculation blurs together different submarkets at the top and bottom of the income spectrum. For example, property in downtown St. Paul in particular is trading hands at steep discounts these days; relative to other central areas, renters can probably find some deals. In a way, it’s the opposite of what you might want to see: declining rents at the top of the market, and increasing rents at the bottom.

Meanwhile, low property values are not good for the city’s bottom line. The study cites the alarming statistic that tax receipts for St. Paul apartments have dropped 27% over the last five years.That amounts to a $40 million hole in sales taxes for the city and county, a sum that other property taxpayers (i.e. single-family homeowners) must make up to meet the overall levies.

The report does end on an optimistic note, claiming that development in St. Paul has likely reached its nadir and has started to improve. That would be welcome news for the city budget and regional density goals. Urban infill remains one of the most effective solutions to climate change, and St. Paul has no shortage of vacant lots near transit lines. If investors begin financing development in St. Paul again, slowly but surely investment housing can begin growing.

In the meantime, thanks to city staff and the Minneapolis Fed, there are lots of analytics to pay attention to. Stay tuned.