We get it, some of you have a go-get-’em attitude and an unwavering confidence when it comes to renovations, repairs, and DIY projects around your home. There’s a certain satisfaction in seeing a problem and tackling it yourself without anyone’s help, but sometimes it’s better to swallow your pride and call in reinforcements.

Despite all appearances, our homes are complex and living things. Wires and pipes run through the interior like blood vessels and neurons, the walls and ceiling flex against the ground, wind, and weather. Moisture and microbes can enter through your doors and windows, or be carried in on your clothing, shoes, and skin. Like any living thing, the systems that keep your house healthy need regular maintenance or else they’ll break down.

While there are plenty of DIY projects you can safely and confidently do on your own, without the help of professionals or even friends, there are other jobs that you probably never want to do solo. Some residential ailments respond well to DIY repairs, while a trained expert better handles others. If you’re facing any of the following projects, take a minute to reconsider before you jump in all by yourself. You probably want to have a friend for reinforcements at the very least, and you might want to consider calling in the pros.

Remove old insulation

Snide12/Shutterstock

If your home was built before the 1980s, there’s a decent chance asbestos insulation is somewhere inside of it. Asbestos is the common name given to the minerals amosite, chrysotile, crocidolite, tremolite, actinolite, and anthophyllite. These minerals occur naturally in rocks and soil; they contain strong fibers that can be spun or woven and are heat-resistant. Consequently, asbestos minerals have been used in a wide range of products.

In decades past, asbestos was commonly used in building insulation and as a flame retardant. It can also be found in vinyl floor tiles, shingles, hot water pipes, furnaces, and more. You can also find it outside the home in friction-based items like brake pads. At home demolition work and renovations are common sources of asbestos exposure. When those materials are disturbed, microscopic asbestos fibers get into the air. Anyone who breathes in those fibers is at risk of lung cancer, mesothelioma (cancer of the lining around the lungs and other organs), asbestosis, a progressive lung disease, and other respiratory diseases.

If you suspect there are asbestos-bearing materials in your home, it’s best to let a professional handle the removal, especially in an enclosed space where exposure to hazardous materials can be greater.

Removing interior walls

Photology1971/Shutterstock

These days, it’s not uncommon to think about knocking down an interior wall or two to give yourself a more open floor plan, but you should probably think twice before you break out the sledgehammer. The Occupational Safety and Health Administration (OSHA) outlines safety requirements for tearing down walls, which can serve as guidelines for at-home DIY projects.

Among those recommendations, OSHA requires that no load-supporting wall be cut or removed unless there’s nothing above it, or every floor above it has already been demolished. Additionally, retaining walls can’t be removed unless the earth they’re retaining has been braced in advance. Unless you’re certain that a wall isn’t structurally important, you should probably think twice before knocking it down.

On top of the structural risks of interior demolition, knocking down walls can also expose you to some yucky things like mold and asbestos. Not so long ago, asbestos was used in things like insulation, soundproofing, joint and patching compounds, textured paint, and more. Knocking down an old wall could unintentionally turn your air into a microscopic minefield. As fun as it can be to turn a wall into smithereens, it’s risky enough to leave to the pros.

Removing mold

amedeoemaja/Shutterstock

Mold and mildew are common problems inside homes, especially in more humid areas. It’s also common when your home experiences leaky pipes or flooding. Mold is part of nature’s cleanup crew, breaking down dead plants and other materials. Microscopic spores floating in the air can set up shop if they find a moist spot. It’s pretty much impossible to keep mold out of your house completely, but you can manage it by keeping things dry and clean.

A major factor in whether you should deal with a mold problem yourself or call in the pros is the scale of the problem. If mold covers less than 10 square feet of your home, it’s probably safe for you to clean it yourself with bleach or detergent. When cleaning up mold, it’s important to protect your lungs with an N95 respirator, protect your skin with gloves, and protect your eyes with goggles or a face shield. Disturbing mold can kick spores into the air, so you’ll want to protect your body on as many fronts as possible.

If your home becomes infested with mold, it could be hazardous to your health, especially for people with allergies, a suppressed immune system, or pre-existing respiratory conditions like asthma or COPD. Possible health impacts include sneezing, a runny nose, eye irritation, skin irritation, and more. If there’s more than a small spot of mold in your home, removal might be best handled by professionals.

Major plumbing jobs

Rafa Jodar/Getty Images

The invention of indoor plumbing is, perhaps, one of humanity’s greatest achievements. Consistent access to clean water and reliable wastewater removal are crucial to health and safety, but they can be easy to take for granted. If your pipes suddenly stop working the way they’re supposed to, it can throw your life into turmoil.

With a little education and patience, you can probably handle DIY plumbing jobs like a leaky faucet, but the larger the job, the more likely you are to encounter complications and benefit from a professional’s assistance. If a plumbing problem isn’t resolved quickly and correctly, even small problems can lead to a host of larger problems down the line, including, but not limited to, sewage coming up your drains, mold, structural damage, and more.

If you’re dealing with outside pipes, like the water intake or your backyard hose/sprinkler system, a broken pipe might not be a huge deal, but inside your home it can be a nightmare. The Better Business Bureau recommends calling an accredited professional anytime a problem threatens your health and safety (some leaky pipes carry contaminated waste water), comfort and sense of security, or your home’s value.

Roof repairs

Jacquesdurocher/Getty Images

A typical roof isn’t necessarily a complicated object. Usually, it’s little more than a wooden frame, some insulation, protection layers like an ice and water shield and underlayment, and shingles to cover everything. If you have a leak you might be tempted to find and fix it yourself.

You’ll want to understand the anatomy of your roof before jumping in, which can vary based on the type of home you have, your location and climate, and even your roof’s slope. Once you know what you’re up against, you’ll also need to choose your repair materials, some of which are toxic and potentially dangerous. Just because a roof is simple doesn’t mean fixing one is. And, of course, there’s always the risk of fall injuries. Climbing onto your roof is inherently dangerous without the right safety equipment.

If you have a small leak, it could be simple enough to fix on your own, in theory, but you probably shouldn’t risk it. While a DIY roof repair can save you some money in theory, it could quickly become more complicated than you expect. And if you don’t get it right, it could lead to worsening leaks, mold growth, water damage, and more.

India’s financial sector is at a turning point. Gross NPAs of Scheduled Commercial Banks have fallen to a historic low of 2.15% as of September 2025, a figure not seen since 2010–11. Yet in absolute terms, gross NPAs still stand at approximately ₹4.32 lakh crore. The scale of the problem hasn’t disappeared; it’s shifted, from large corporate defaults to a more distributed mass of retail and MSME accounts scattered across geographies, legal jurisdictions, and ticket sizes.

For banks, NBFCs, and fintechs trying to recover these dues, understanding India’s debt recovery laws is not optional, it is foundational. This guide breaks down every major legal channel available, how they perform in practice, and what 2025’s regulatory shifts mean for lenders and recovery professionals.

At a Glance: India’s debt collection software market reached approximately $172.8 million in 2024 and is projected to reach $456 million by 2033 (CAGR of 10.48%, IMARC Group). Over 320 new debt recovery platforms launched between 2022 and 2024. The race is on, but legal infrastructure remains the backbone.

What Is Debt Recovery?

Debt recovery is the structured process by which lenders reclaim unpaid loan amounts from borrowers who have defaulted. Credit creation, through loans extended to individuals, MSMEs, and corporations, is essential to economic growth. But when borrowers default, lenders must navigate a complex web of legal mechanisms to recover what is owed. In India, this ecosystem spans eight distinct legal frameworks, multiple tribunals, and an increasingly digitised regulatory environment.

A loan account is classified as a Non-Performing Asset (NPA) when both principal and interest payments remain overdue for 90 days. Once classified as an NPA, lenders have access to several legal channels to recover dues, each with its own jurisdiction, timelines, and effectiveness.

Two Paths: Legal vs. Illegal Methods

The law draws a clear line between legitimate recovery and harassment. RBI guidelines require that all recovery communications occur strictly between 8 AM and 7 PM, agents carry valid identification, and no abusive or intimidatory tactics are used. The RBI’s February 2026 draft directions for both commercial banks and AIFIs (All India Financial Institutions) now mandate board-approved recovery policies, IIBF certification for agents, recording of recovery calls, and public disclosure of empanelled recovery agents, all effective July 1, 2026.

Illegal methods, public shaming, threats, late-night calls, or unauthorised property seizure, are not only unethical but expose lenders to regulatory action and grievances filed with the RBI Ombudsman. Nearly 39% of borrowers surveyed have reported abusive recovery calls; RBI data confirms that loan and credit-card complaints now form the largest single category of grievances received.

The 8 Legal Methods of Debt Recovery in India

1. Indian Contract Act, 1872

Every loan relationship originates from a contract. If a borrower defaults, the lender can seek legal relief under several provisions of the Indian Contract Act, through a Contract of Guarantee (Section 126), Contract of Indemnity (Section 124), or by establishing Fraud (Section 17) or Misrepresentation (Section 18). This is typically a foundational step before more specific recovery mechanisms are invoked.

2. Civil Remedy (CPC Order IV)

A civil suit under Order IV of the Civil Procedure Code allows lenders to approach a court for money recovery. The suit must be filed within 3 years from the date of the cause of action and in the court that has jurisdiction over the borrower’s residence or place of business. Court fees are levied based on the claim amount. Civil suits are best suited for cases where other faster mechanisms are not available — but they are time-consuming and should be approached with a structured documentation trail.

3. Criminal Case Under IPC (Now BNS, 2023)

Where the default involves elements of cheating, criminal breach of trust, or dishonest misappropriation, lenders can file a criminal case. Key provisions include Cheating (Sections 415/417 IPC, now mirrored in the Bharatiya Nyaya Sanhita, 2023), Criminal Breach of Trust (Sections 405/406), and Dishonest Misappropriation of Property (Section 403). Some of these offences are non-bailable and cognizable, meaning the defaulter faces serious legal consequences.

4. Insolvency and Bankruptcy Code (IBC), 2016

The IBC remains India’s most powerful corporate debt recovery instrument. Where the defaulted amount exceeds ₹1 crore (revised from ₹1 lakh in 2020), creditors can approach the NCLT for initiating the Corporate Insolvency Resolution Process (CIRP). A Committee of Creditors (CoC) is formed, an Insolvency Professional appointed, and the resolution must be approved by 66% of CoC votes within 330 days.

IBC Impact by the Numbers (as of March 2025): — Over 30,000 applications involving defaults of ₹13.78 lakh crore were settled at the pre-admission stage alone, demonstrating IBC’s deterrence effect. — Average recovery rates improved from 15–20% pre-IBC to approximately 30% post-IBC (S&P Global Ratings, December 2025). — S&P upgraded India’s insolvency regime from ‘Group C’ to ‘Group B’ in December 2025. — However, actual average CIRP duration stands at 713 days, more than double the statutory 330-day limit. NCLT pendency is nearly 30,600 cases (March 2025), with an estimated 10-year clearance time at current rates.

IBC’s biggest strength is its behavioural impact, it has fundamentally shifted the culture from “debtor in possession” to “creditor in control.” The proportion of overdue corporate loan amounts relative to total outstanding fell from 18% in 2018 to 9% in 2024 (IIM Bangalore study).

One of the most frequently invoked debt recovery provisions in India, Section 138 of the NI Act applies when a post-dated or security cheque issued by a borrower is returned unpaid. Upon dishonour, the payee must send a demand notice within 30 days; if the borrower fails to make payment within 15 days, criminal proceedings can be initiated. The defaulter may face imprisonment of up to 2 years, a fine twice the cheque amount, or both. Cheque bounce cases number in the millions annually across Indian courts, making efficient case management critical for lenders handling high volumes.

The Recovery of Debts Due to Banks and Financial Institutions Act established a network of 39 Debt Recovery Tribunals (DRTs) and 5 Debt Recovery Appellate Tribunals (DRATs) across India. Banks and NBFCs can file applications under Section 19 for recovery of dues. Borrowers who wish to appeal a DRT order must deposit 50% of the debt amount (reducible to 25% by the appellate tribunal). While DRTs were designed for speed, chronic understaffing and high pendency have limited their effectiveness. DRTs accounted for just 4.2–4.9% of total NPA recovery in recent years, among the lowest of all channels.

Note on DRT Reform: The government has signalled intent to expand DRT jurisdiction and address vacancies. The BAANKNET e-auction portal, launched March 25, 2025, is already improving asset disposal efficiency for PSBs and IBBI-referred cases.

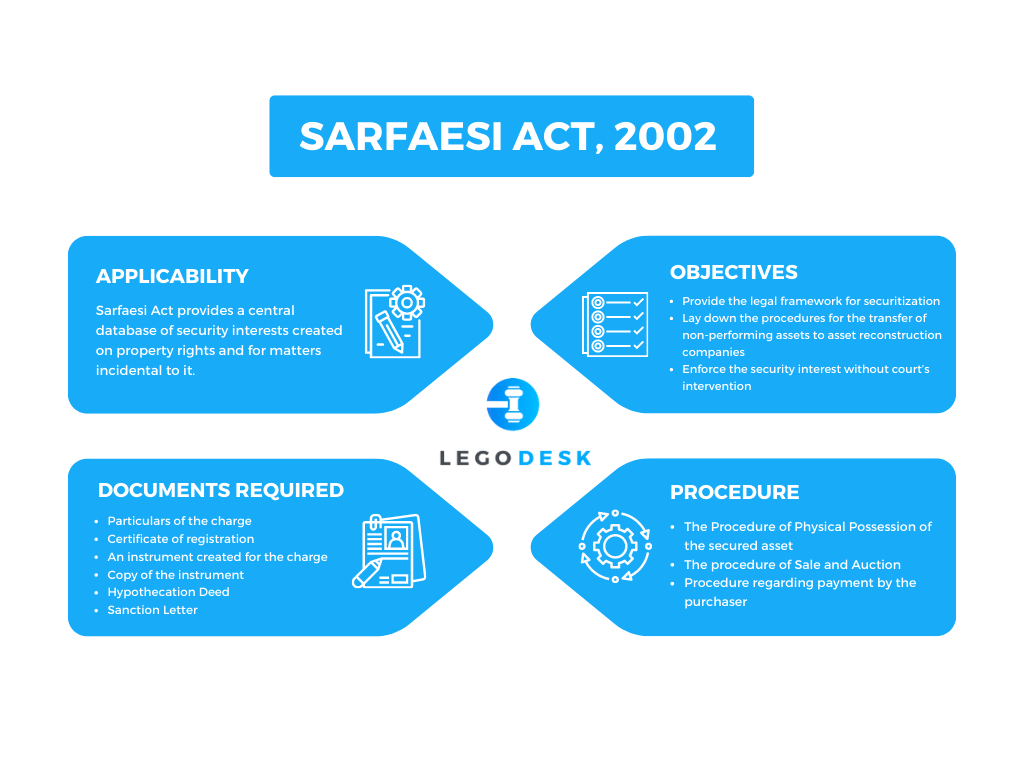

7. SARFAESI Act, 2002

The Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act allows secured creditors, banks, NBFCs, and ARCs, to take possession of and sell secured assets without court intervention. Once a loan is classified as NPA under Section 13, a notice is sent to the defaulter giving 60 days to repay. If repayment doesn’t happen, the lender can sell the asset or assign it to an Asset Reconstruction Company (ARC) at a discounted rate.

SARFAESI is particularly favoured by banks due to lender control over the asset sale process. It accounted for 17.4–26.7% of total NPA recovery in recent reported years. Recent amendments have strengthened the framework further, including empowering RBI to audit ARCs and mandating CERSAI registration of security interests.

8. Summary Suit

A Summary Suit (Order XXXVII, CPC) is a fast-track civil proceeding suited for liquid debts not exceeding ₹10 lakh. The defaulter has just 10 days from the date of service to appear before the court. If they fail to do so, the court may pass an ex-parte decree immediately. While the ticket-size cap limits its use for large institutional lending, it is a practical tool for smaller NBFC or retail exposures.

How Each Channel Actually Performs: Recovery Rate Comparison

Recovery Channel

Share of Recovery (Recent Years)

Average Timeline

Best Suited For

IBC / NCLT

~44–46% (highest among all channels)

713 days average (statutory: 330 days)

Large corporate defaults >₹1 crore

SARFAESI Act

17–27%

Months (no court required)

Secured assets, banks & larger NBFCs

DRTs

4.2–4.9%

1–3+ years (due to pendency)

Mid-size bank/FI claims

Lok Adalats

~6% (low recovery per case)

Weeks to months

Small-ticket pre-NPA settlements

Section 138 / NI Act

Varies (high volume, lower value)

1–3 years in metro courts

Cheque-secured loans

Civil Suits

Varies

3–7 years

Unsecured creditors, contractual disputes

Sources: RBI Annual Reports, IBBI data, Lexology analysis, IBC Laws research platform, FACTLY data analysis (March 2025).

RBI’s 2025–26 Guidelines: What’s Changing for Lenders

The regulatory landscape for debt recovery shifted significantly in 2025. Three key developments stand out:

1. RBI Digital Lending Directions, 2025 (effective May 8, 2025) — This consolidated framework governs all digital lending activity including recovery. Lenders must notify borrowers via email/SMS before any recovery agent makes contact, ensure all disbursals go directly to borrower bank accounts, and maintain transparent grievance channels. Lending Service Providers (LSPs) acting as recovery agents are now held to the same standards as the Regulated Entity (RE) itself.

2. Draft Responsible Business Conduct (Amendment) Directions, February 2026 — Released simultaneously for commercial banks and AIFIs, these draft directions (effective July 1, 2026) represent the most comprehensive overhaul of recovery conduct standards in years. Key mandates include: board-approved recovery policy, IIBF certification for all recovery agents, mandatory recording of recovery calls, public disclosure of empanelled agents, written notice of default before any recovery action, and strict prohibition on harsh practices including public shaming, abusive language, and family/colleague harassment.

3. BAANKNET Portal, March 2025 — The government’s revamped e-auction platform integrates all 12 Public Sector Banks and IBBI with automated KYC, secure payments, and bank-verified property titles, significantly improving transparency in SARFAESI-based asset sales.

Compliance Implication for Lenders: Legal recovery today is increasingly about process documentation, not just legal filing. A timestamped, digitally-traceable record of every notice, communication, and action is no longer just operationally helpful — it is a regulatory requirement. A WhatsApp chat archive will not hold up under RBI or DRT scrutiny.

Best Practices for Lenders Navigating the Legal System

Build a Structured Internal Process Before Filing

Debt recovery requires coordination across internal legal, finance, and collections teams — and often, an external advocate or law firm. Designate clear accountability: who signs the notice, who coordinates with external counsel, who monitors hearing dates. Manual calendar-based tracking of court dates leads to adjournments, value erosion, and missed opportunities. Automated case management — with alerts triggered by hearing schedules, advocate assignments, and SLA breaches — is the baseline for any serious recovery operation today.

Document Everything, Digitally

Every communication with the borrower — from the first demand notice to field visit reports — must be documented with timestamps. This is not just good practice; it directly affects your legal standing. In SARFAESI and DRT proceedings, the quality and completeness of the paper trail often determines outcomes. Automated notice dispatch that generates a delivery-confirmed, timestamped audit log gives lenders a defensible record.

Choose the Right Jurisdiction Before Filing

Filing in the wrong court or tribunal is a costly, time-consuming error. Match the legal channel to the debt type and ticket size: IBC/NCLT for large corporates (>₹1 crore), SARFAESI for secured assets, DRT for bank/FI claims, Section 138 for cheque bounce, civil suits or Lok Adalats for smaller unsecured accounts. For retail and MSME NPA accounts with smaller ticket sizes, pre-litigation ODR (Online Dispute Resolution) platforms are emerging as a cost-effective alternative to formal proceedings.

Engage Qualified Counsel, and Track Their Performance

Advocate selection in recovery litigation is frequently based on familiarity rather than performance data. This leads to systemic underperformance. High-performing lenders are increasingly using data to track advocate win rates, adjournment frequency, and case resolution timelines by jurisdiction, and adjusting their panels accordingly.

Maintain Ethical Standards to Protect Your Recovery

Courts and tribunals look at the conduct of both parties. A lender that can demonstrate ethical, documented, and RBI-compliant recovery behaviour before filing is better positioned to receive favourable outcomes. Violations of RBI conduct guidelines, even if not the direct subject of the case, can undermine a lender’s standing.

The Role of Technology in Modern Debt Recovery

The 2024–25 period has seen a structural shift in how lenders approach recovery infrastructure. AI is now deployed across predictive default scoring, omnichannel borrower communication, automated legal notice dispatch, and court case management. Mid-sized banks have reported a 34–36% reduction in collection costs after AI adoption, with recovery rate improvements of 10–25%.

The most significant strategic shift is toward ecosystem thinking rather than monolithic platform adoption. Different parts of the recovery journey require different tools: pre-litigation communication platforms for early-stage accounts, ODR/mediation for small-ticket disputes, and dedicated legal operations infrastructure for NPA accounts heading to DRT, SARFAESI, or NCLT. The bridge between collections-stage activity and legal-stage activity, where cases are handed off, documents compiled, and notices issued, remains the most operationally fragile point in most lenders’ recovery chains.

Key Technology Stats for Recovery Professionals: — AI adoption in mid-size banks: 34–36% cost reduction in collections — Recovery rate improvement post-AI: 10–25% — India’s debt collection software market CAGR: 10.48% (2024–2033) — PSB gross NPA ratio: 2.50% (September 2025) — Private sector bank NPA ratio: 1.73% (September 2025)

The Bottom Line

India’s debt recovery legal framework is comprehensive, and under active improvement. The IBC has reshaped creditor rights. SARFAESI gives secured lenders direct enforcement power. The 2025–26 RBI guidelines are tightening conduct standards while pushing for digital accountability. And the absolute scale of NPAs, despite improving ratios, means the demand for effective, tech-enabled, legally defensible recovery will only grow.

For lenders, the question is no longer whether to digitise their legal recovery operations, but how quickly they can build infrastructure that is compliant, data-driven, and defensible at every stage, from first notice to final court order.

Want to see how Legodesk connects your collections workflow directly to legal recovery, from automated notice dispatch to court case management, notice tracking, and recovery through Lok adalat? Request a demo

To provide the best experiences, we use technologies like cookies to store and/or access device information. Consenting to these technologies will allow us to process data such as browsing behavior or unique IDs on this site. Not consenting or withdrawing consent, may adversely affect certain features and functions.

Functional

Always active

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.