Chrysler’s HEMI is one of the most recognizable names in automotive history, its reputation built primarily on the iconic 426 HEMI that powered muscle cars like the Dodge Charger R/T and Plymouth HEMI ‘Cuda. But the 426 was also incredibly short-lived, only made available as a street car engine from 1966 to 1971; after that, production HEMI engines were essentially dead, the name lying dormant for the better part of three decades until Chrysler revived the branding with the Gen III 5.7 HEMI for the 2003 model year.

In the years after that, the revived HEMI made its way to a series of vehicles under the DaimlerChrysler — later Chrysler, then Fiat Chrysler Automobiles, then Stellantis — umbrella, including modern-day Mopar legends like the Dodge Challenger R/T and more family-friendly offerings like the Dodge Durango and Jeep Grand Cherokee. Along the way, the Gen III HEMI family also expanded to include a range of bigger and badder engines such as the 6.2-liter supercharged Hellcat engine, one of the most powerful HEMI engines ever made.

While there’s no way around the fact that it’s those big-power modern HEMIs that are the most exciting ones to discuss, they arguably would never have existed had the 5.7 HEMI (and the vehicles that it powered) not captured fans and admirers the way they did. And so, let’s take trip down memory lane and look at some of the 5.7 HEMI’s greatest hits.

Ram pickups

While the HEMI name may be indelibly associated with high-performance motoring thanks to the 426, the Gen III 5.7 HEMI’s beginnings were far more humble. The revived engine first debuted under the hood of the third-gen Dodge Ram 1500, 2500, and 3500 pickups, coming a year or so after they hit the streets for the 2002 model year.

The 345-hp V8 came to the heavier-duty Ram 2500 and 3500 pickups first, but became available in the Ram 1500 by the time 2003 rolled around. In the Ram 1500, the HEMI replaced the 245-hp, 5.9-liter Magnum V8 as the top-dog engine option, offering a significant bump in power for a not-unreasonable extra $795. Conversely, the HEMI was the standard option for the heavy duty (HD) trucks, with a larger 8.0-liter V10 and a handful of Cummins turbodiesels also available.

Dodge’s 5.7-liter engine eventually became a fixture in the Ram pickups’ engine bays. Dodge introduced the the Multi-Displacement System (MDS)-equipped version of the engine for the 2009 model year (which came with a welcome bump in power to 390 hp in the Ram 1500) and the engine continued to be available for at least another decade. The HD trucks dropped the 5.7 in favor of the 6.4-liter in 2019, but the former was available in the Ram 1500 until the 2024 model year, after which Dodge discontinued the HEMI — but only briefly. After one HEMI-less year in 2025, Ram brought the engine back for the 2026 Ram 1500 to great sales success, although some (including us) don’t think the HEMI-equipped 2026 Ram 1500 is actually all that great.

Dodge Charger R/T

Dodge’s Ram pickups were perhaps not the most traditional place to debut the revived HEMI, but the engine quickly made its way to other vehicles after its first outing. Pretty soon, the automotive world would get a proper muscle car flashback when Dodge brought the HEMI and Charger back together for the 2006 model year.

That year, Dodge debuted a revived Charger that rode the same retro-futuristic wave as the 2005 Ford Mustang, retaining classic muscle car tropes — a 340-hp HEMI in the Charger R/T and rear-wheel drive — but with a dose of practicality. To that end, the Charger was a full-on sedan, with four doors and modern features like a manual-capable auto gearbox and traction and stability control to keep things in check. It echoed its ’60s and ’70s forebears in some of the design touches, but was otherwise a modern muscle car for the then-modern buyer — all for a roughly $30,000 price that journalists were particularly keen on.

As with many of its 5.7-powered brethren, the Charger R/T would have the V8 in the engine bay for the rest of its run. It received the updated MDS-capable version of the 5.7-liter in 2009, which made 368 hp – climbing ever so slightly to 370 hp when the all-new seventh-gen Dodge Charger debuted for the 2011 model year. Dodge kept the 5.7 around for the rest of the run, introducing the 5.7-powered Charger Daytona in 2013, until it dropped internal combustion with the Dodge Charger Daytona EV in 2024 — although there are strong indications that it’s bringing the V8 back in the future.

Chrysler 300

Chrysler may be a shadow of its former self, with only two minivans — the Pacifica and Voyager — in its lineup at the time of writing, but there was a time when the brand had much more exciting fare to offer. Case in point: the Chrysler 300.

The 300 — whose name was chosen to echo the Chrysler 300 “Letter Car” models from 1955 to 1965 — was first unveiled as the 300C concept car in 2003. Chrysler had already decided that it would use the then-new HEMI V8 at that point — the first HEMI to grace a Chrysler engine bay in over 40 years, in fact, according to a press release accompanying the concept. It didn’t stay a concept for long, though, and Chrysler brought 300 to market in 2004 for the 2005 model year.

Available in several guises ranging from the 190-hp, V6-powered Chrysler 300 up to the 340-hp, HEMI-equipped 300C, the big sedan was an instant hit with consumers and critics alike: It sold more than 100,000 units in each of its first three years and won accolades like the North American Car of the Year award in its first year. It shared the LX platform with the front-engine, rear-drive Dodge Charger, and continued to do so when Chrysler moved to the LD platform in 2011. The platform change brought a wide range of updates, but one thing that didn’t change (aside from a bump in power to 363 hp) was the 5.7 HEMI, which stayed as an option all the way until the end of the line in 2023.

Dodge Challenger R/T

If we had to single out one vehicle that has flown the flag for the Gen III HEMI engine in all its guises, it’s likely the Dodge Challenger. The resurrected nameplate debuted in 2009 as an aggressive, retro-minded two-door coupe that took the existing Dodge Charger and Chrysler 300 platform in an exciting new direction — and established itself as a modern-day Mopar legend in the process.

The 2009 Challenger was available in three versions: the SE, which had a 250-hp V6; the R/T, which had the revised 5.7-liter HEMI with 372 hp (or 376 with a manual transmission); and the SRT8, equipped with the 425-hp 6.1-liter HEMI that was the top dog in Dodge’s arsenal at the time. The SRT8 would eventually be dethroned by the first Challenger Hellcat in 2015, kicking off a chain of increasingly powerful variants of the car (and the Gen III HEMI), but the 5.7-liter would continue trucking along as the entry-level V8 option up until Dodge discontinued the Challenger at the end of the 2023 model year.

The R/T’s 5.7-liter HEMI is never going to be the highlight of the model’s nearly 15-year run, but it served its purpose, and reviewers of the time thought it was more than adequate — especially considering its fuel economy advantages over the SRT8. The Challenger sold more than 50,000 units yearly for much of its life, and we wouldn’t be surprised if the R/T’s charms played a big role in its strong sales.

Dodge Durango

The Charger and Challenger R/T may be the most recognizable modern Dodge vehicles to have the 5.7-liter HEMI under the hood, but the Durango ranks above both of those in terms of sheer HEMI-powered longevity. So while it’s never going to set the heart racing like a Challenger R/T, the Durango is undoubtedly another one of the engine’s greatest hits.

The HEMI-powered second-gen Durango joined the Dodge lineup for the 2004 model year, with the engine slotting in at the top of the pecking order above a 3.7-liter V6 and 4.7-liter V8, both from Dodge’s older Magnum engine family. The Gen III HEMI made 330 hp — quite mundane now that we have 500-plus-hp SUVs, but strong in 2004 — and the automaker expected it to account for the majority of the second-gen Durango’s sales. Dodge’s bet seemed to have paid off; it sold more than 100,000 Durangos in its first year, though the late-2000s financial crisis forced Chrysler to discontinue the model after 2009.

Dodge didn’t leave the Durango nameplate on ice for too long, though. The automaker announced the triumphant return of the Durango to the lineup in 2011, with the 5.7-liter HEMI in tow, of course. Like its HEMI-powered siblings, the new SUV got the improved, variable valve timing (VVT)-capable version of the engine, which made 360 hp. Unlike those siblings, however, the Durango kept hold of the HEMI — in 6.4- and 5.7-liter configurations — even after Dodge stopped offering it in other models. The automaker went one step further in 2026, too, making the 5.7-liter V8 the standard engine in the entry-level Durango GT.

Jeep Grand Cherokee

The Jeep Grand Cherokee is one of the longest-lived models in the current Jeep lineup: As of 2026, there have been five generations of the Grand Cherokee since it debuted in 1993. The 5.7-liter HEMI was the powerplant in the Grand Cherokee’s engine bay in 2005, alongside the SUV’s third generation, and was an option through two full generations plus the first few of a third.

Jeep’s third take on the Grand Cherokee featured a range of improvements that gave it even better off-road credentials, including low-range gearing and a Quadra-Drive II system with electronic limited-slip differentials, but the highlight was most likely said HEMI. The 5.7-liter V8 joined the party alongside a similarly-new 3.7-liter V6 with 210 hp and a 4.7-liter V8 producing 235 hp. The HEMI was way out in front of the Grand Cherokee’s other engines in terms of power output, with a stout 330 hp available.

A new Grand Cherokee debuted in 2011, which again came with the 5.7-liter HEMI as an option. Power was up across the board, with the HEMI now making 360 hp and the base Pentastar V6 making a healthy 290 hp. Both of these were still available for the fifth generation, which debuted in 2021 — by which point the 5.7-liter HEMI had been joined by its 6.4-liter and Hellcat siblings. This wasn’t for long, though; Jeep dropped all the V8s in favor of the Pentastar V6 starting in 2024. That V6 had the engine bay to itself for a couple of model years, but that changed with the introduction of Stellantis’ brand-new, 324-hp Hurricane 4 Turbo engine in the 2026 Jeep Grand Cherokee.

There’s a popular argument that AI will do to human workers what tractors did to horses. Tractors could do what horses did. Horses became obsolete. AI can do what humans do. Therefore…

Plenty of major AI figures seem to agree. Elon Musk says AI will “replace all jobs.” Anthropic CEO Dario Amodei regularly warns about mass job loss, framing AI as “a general labor substitute.” OpenAI investors talk openly about AI replacing “80% of all jobs by 2030.” These are influential people, not random bloggers. Still, they are not necessarily a representative sample of the world’s most careful economists.

And the fear itself is hardly new. Economist Wassily Leontief—best known for developing input-output analysis, a way of mapping how industries depend on one another—raised similar concerns in the early 1980s. If AI really were a perfect substitute for human labor, the logic would be straightforward. Any cost advantage would eventually drive firms toward 100% AI labor. You do not need a long essay to prove that result.

The problem is that the phrase “AI will eventually be a perfect substitute” does almost all the analytical work. That assumption hides a great deal: differences across tasks, industries, and workers; the many margins along which firms adjust; and the messy heterogeneity that makes the real economy more than a toy model.

How substitutable is AI today? What would need to happen for that substitutability to rise meaningfully? What other conditions would also need to hold? Even the historical analogy—“tractors could do what horses did, therefore horses became obsolete”—compresses several distinct steps into one neat sentence. “AI can do what humans do, therefore humans become obsolete” hides even more.

So let’s unpack those steps.

(This post draws on a new working paper that walks through the math and economics in detail. Really, though, it is mostly basic accounting.)

Before We All Become Horses

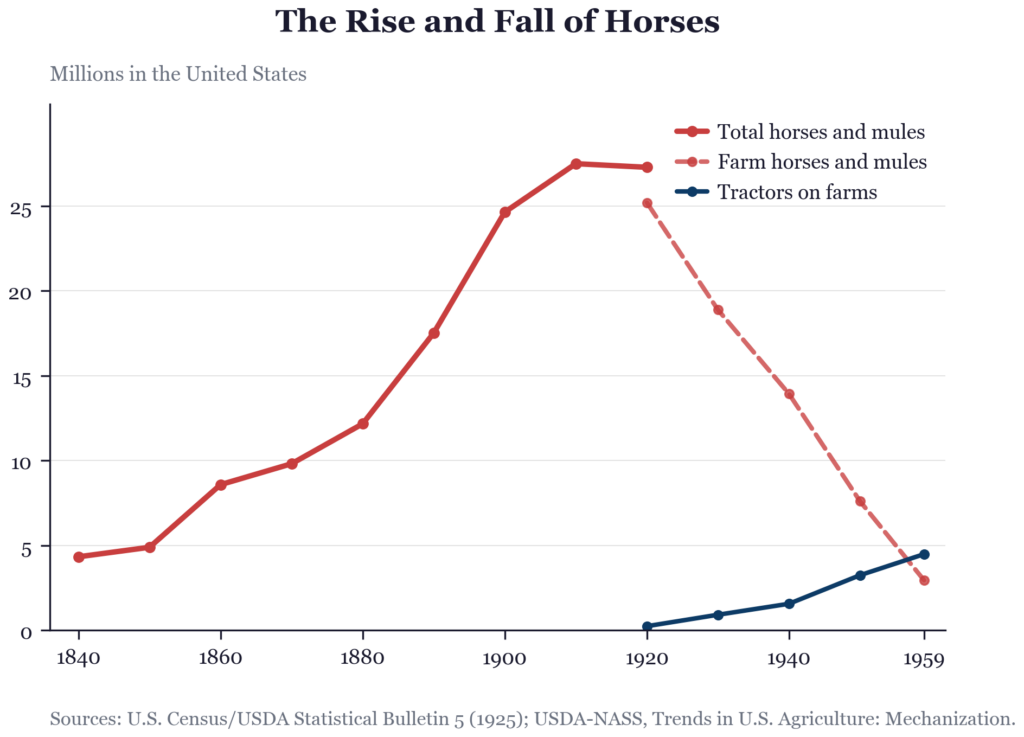

For those unfamiliar with the history of horses in the United States, the horse population actually rose for decades alongside industrialization. It increased from 4.3 million in 1840 to 27.3 million in 1920. The collapse came later, as tractors and motor vehicles displaced horses in agriculture and transportation. The number of farm horses and mules then fell to roughly 3 million by 1960.

Horses, in effect, had one main economic role, and that role disappeared. Humans are different. So before jumping from “AI can do tasks” to “humans become obsolete,” we should define carefully what that outcome would actually mean.

To keep things simple, suppose demand for human labor falls to zero. Not “low.” Zero. What would that require?

It would mean that no dollar spent anywhere in the economy passes through human labor at any point in the supply chain. Not the person who made the product. Not the person who shipped it. Not the person who designed it, marketed it, maintained it, or cleaned the building where it was assembled. Zero human labor embodied in final expenditure. That is the benchmark. That is what “humans become horses” would mean, stated precisely.

This is the input-output framework the aforementioned Wassily Leontief built his career on. The idea is straightforward: trace any final purchase backward through its supply chain and add up all the labor that contributed to it, both directly and indirectly. A cup of coffee includes the labor of the barista, but also the roaster, the truck driver, the coffee farmer, and the workers who built the truck. “Embodied labor” means all of it.

For labor demand truly to collapse, every one of those links would need to disappear across every good and service consumers buy. That is a much stronger claim than “AI can do some jobs.” The economy is not a single production function. It is a sprawling network of activities. When AI makes one activity cheaper, consumers do not simply buy more of the same thing forever. They redirect spending elsewhere.

Every dollar lands somewhere. Some spending flows into highly labor-intensive activities, such as restaurants, therapy, or home repair. Other spending flows into activities that require very little labor, such as cloud storage, automated checkout systems, or streaming subscriptions. So the relevant question is not merely: “Can AI do my job?” It is: “When AI makes some things cheaper, where does the saved money go next?”

Aggregate labor demand depends on at least three things: total spending in the economy, the share of spending that goes toward labor-intensive activities, and the amount of labor embodied in each activity. For labor demand to fall to zero, AI cannot merely displace workers in a few sectors. Every dollar of spending, wherever it ultimately lands, must shed all embodied human labor. The “humans become horses” story therefore requires three separate margins to collapse simultaneously.

A useful starting point is the simple observation that firms do not want labor per se. A restaurant does not want waiters because it enjoys employing waiters. It wants orders taken, customers reassured, mistakes fixed, and meals delivered. Labor demand is therefore “derived demand”—firms demand workers because workers help produce something else consumers value.

When AI can perform those underlying tasks more cheaply, two things happen at once. First, firms substitute AI for workers, reducing labor demand per unit of output. Second, lower production costs reduce prices, output expands, and that expansion tends to pull labor demand back upward. Whether total labor demand rises or falls depends on which force dominates.

Economists call this the Hicks-Marshall decomposition of derived demand into substitution effects and scale effects. The terminology sounds forbidding, but the intuition is simple: cheaper production reduces the need for workers in one sense, while expanding the market for output in another. That tension will organize the rest of the discussion.

When a dollar gets saved, where does it go? Into new tasks? New jobs? New industries? The money has to end up somewhere.

Your Job Is Not a Checklist

The case that AI can automate many tasks is not speculative anymore. This is obviously true to some extent, and it has been true for years.

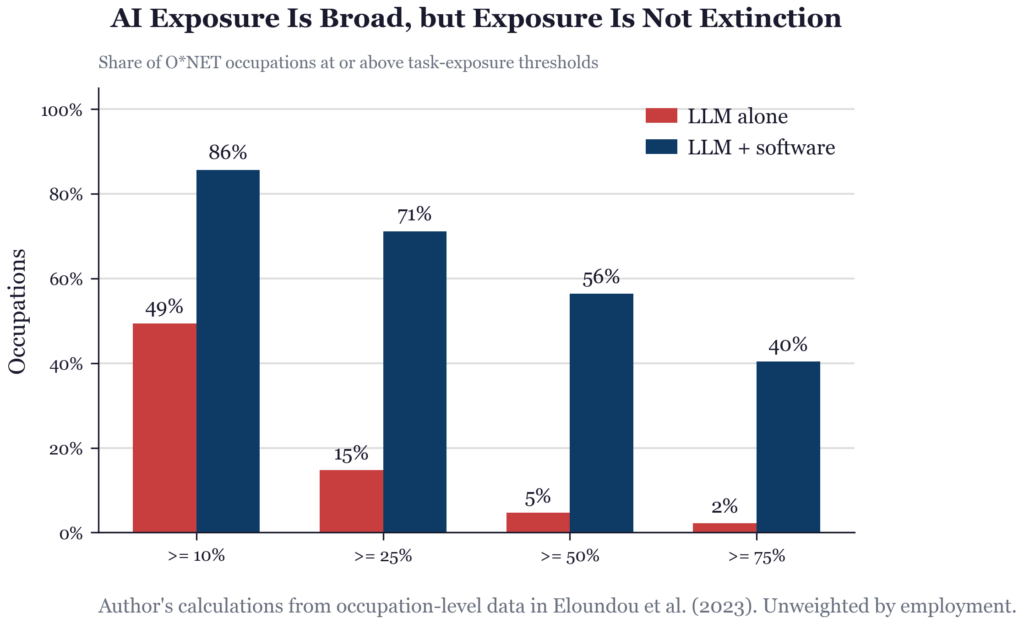

Even early large language models (LLMs) showed substantial potential to affect workplace tasks. One widely cited paper by Tyna Eloundou, Sam Manning, Pamela Mishkin, and Daniel Rock estimated that roughly 80% of the U.S. workforce could see at least 10% of their job tasks affected by LLMs. When paired with complementary software tools, 86% of occupations crossed that 10% exposure threshold.

Since then, the empirical literature has grown rapidly, and the task-level evidence is hard to dismiss. In a large customer-support study, access to generative AI increased the number of issues resolved per hour by roughly 15%. In an experiment involving professional writing tasks, ChatGPT reduced average completion time by 40% while increasing measured output quality by 18%. In a controlled GitHub Copilot study, software developers completed coding tasks 55.8% faster. Those are not rounding errors.

But they are effects on tasks, not necessarily on jobs. That distinction matters. When a task gets automated, the saved dollar does not disappear into the void. Firms and workers often redirect it toward new activities within the same occupation: more client management, more review and verification, more coordination, more judgment calls, more customization.

Just as there is no fixed amount of demand in the economy, there is no fixed bundle of tasks that permanently defines a job. Jobs evolve. They absorb new responsibilities, shed old ones, and reorganize around whatever remains scarce and valuable.

The O-Ring Problem

There is a familiar ritual in AI discourse. Someone posts a demo. The demo performs a task associated with a particular job. People immediately conclude that the job is doomed.

Sometimes they are right. But that inference skips about 15 intermediate steps.

What does it actually cost to deploy the system once error rates are included? Do customers trust it? Can firms reorganize workflows around it? Does management even know how to integrate it effectively? A chatbot demo can appear overnight. A hospital cannot reorganize clinical liability around AI overnight.

That distinction matters because firms are not simply collections of isolated tasks. They are organizations. In many cases, the result will not be pure replacement, but rather a human-AI team producing output together. Economists call this complementarity: two inputs become more valuable when used jointly than separately.

But complementarity is not free. A human-AI pair that produces only marginally more value than the AI alone will not justify paying a full human wage. The human worker must contribute something the AI cannot reproduce cheaply or reliably.

That matters especially in high-stakes settings where errors are extraordinarily costly. Surgery, aviation, structural engineering, fiduciary advice, and many legal services all fall into this category. In these fields, the cost of failure can easily dwarf the savings from cheaper production.

That could eventually change. It probably will change in some areas over time. But it is not likely to change quickly.

This is essentially the “O-ring” logic from economics, named after the tiny rubber seal whose failure destroyed the Space Shuttle Challenger. When the value of the entire system collapses because one component fails, buyers do not focus primarily on sticker price. They focus on the expected cost of a system that actually works.

In those environments, human-supervised production can remain economically efficient even if AI itself becomes extremely cheap.

Horses Had Nowhere Else to Go

Suppose substitution effects really do dominate within most jobs. The saved dollar then escapes the workplace entirely. Where does it go next?

Most standard economic models collapse the economy into a single “final good,” which makes that question disappear by assumption. Real economies do not work that way. They contain many sectors, and every dollar eventually lands somewhere.

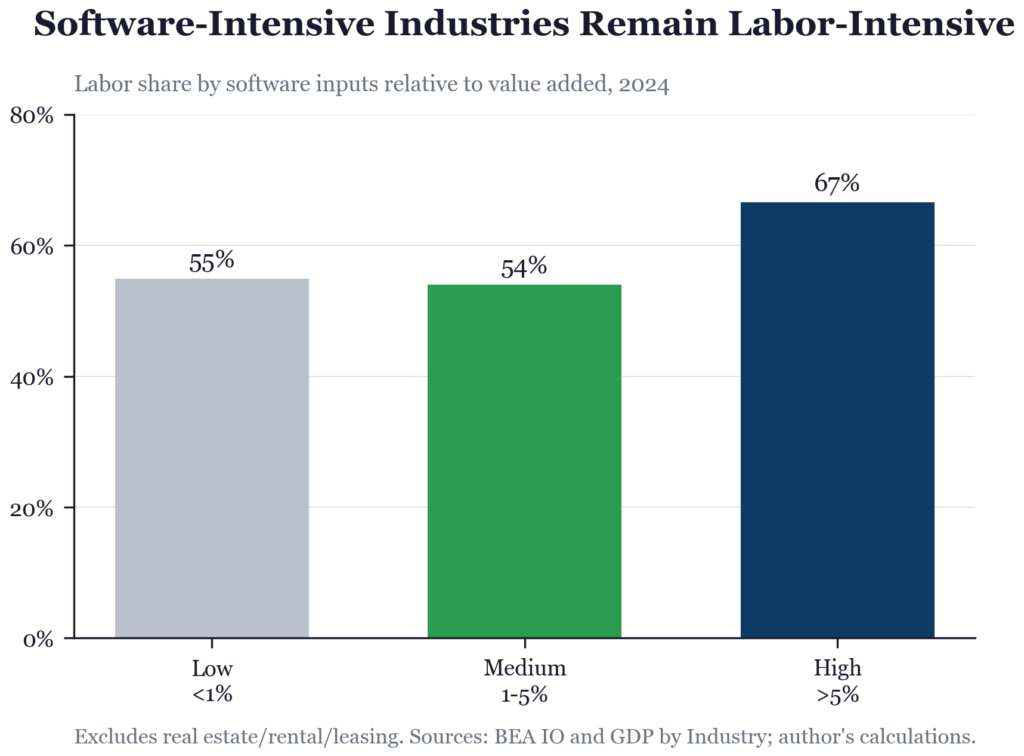

Start with software, which serves as a useful microcosm. Software-intensive industries have already undergone decades of automation through digital tools. If automation were going to drive human labor out of a sector entirely, this is where you would expect to see it first. The chart below groups industries according to how much software they purchase relative to value added: low, medium, and high software intensity. The result is striking.

The most software-intensive industries do not merely retain human labor. They actually devote a larger share of income to labor compensation—about 67%—than the least software-intensive industries, which devote roughly 55%. In other words, the industries that automated the most heavily also remained highly labor-intensive.

The same pattern appears in employment projections. The Bureau of Labor Statistics (BLS) projects total U.S. employment to increase by 5.2 million jobs between 2024 and 2034. Employment for software developers—a profession directly exposed to AI tools—is projected to grow 17.9%. BLS could ultimately prove wrong. Forecasting always carries uncertainty. Still, the evidence so far points strongly toward scale effects dominating in software-intensive industries. Automation reduced costs, output expanded, and labor demand remained robust.

Software may be an extreme case, but versions of this pattern appear across the broader economy and over much longer periods. Take the shift from goods to services. In 1929, most consumer spending went toward physical goods. Today, roughly two-thirds of consumer spending flows toward services. As manufacturing became dramatically more efficient, consumers did not respond by purchasing infinite refrigerators and toasters. Instead, spending shifted toward health care, education, restaurants, entertainment, travel, and personal services.

That is the “saved dollar” in action at the economy-wide level. Goods became cheaper. The substitution effect largely won within goods-producing industries. Employment growth in manufacturing did not continue indefinitely. But the freed-up purchasing power migrated elsewhere, and the scale effect emerged across sectors instead.

From a macroeconomic perspective, output expanded overall. Consumers simply redirected spending toward new categories of consumption. But migration alone does not help workers unless the destination sectors still contain substantial human labor. Did they?

Again, the answer appears to be yes.

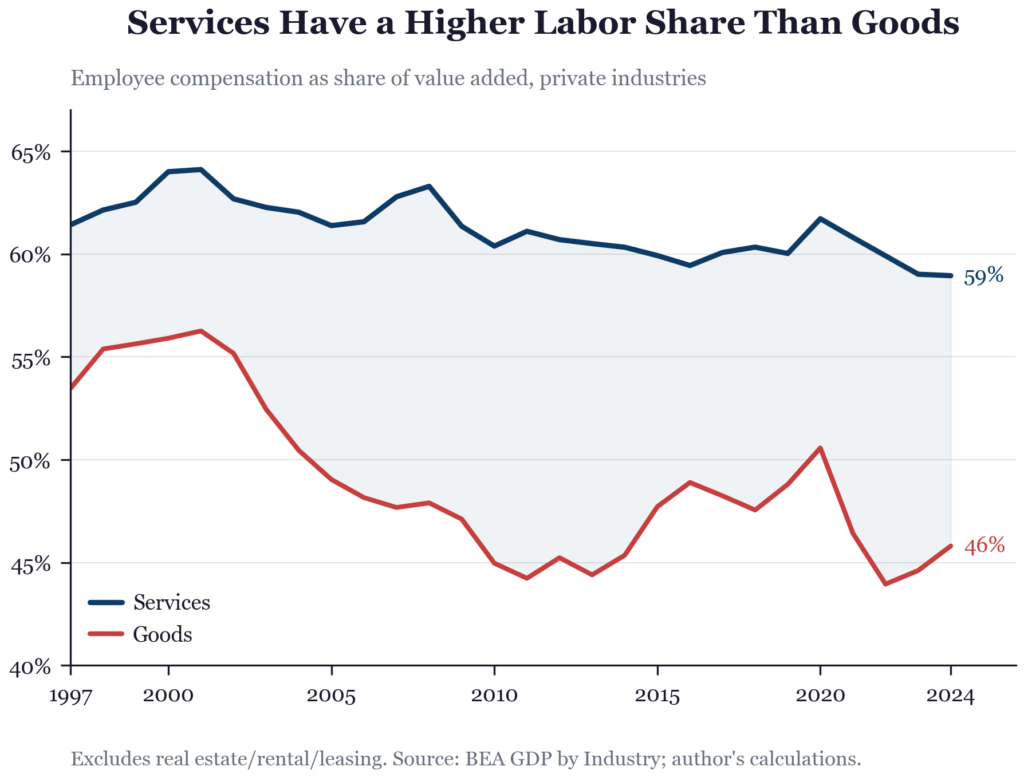

Services consistently devote a larger share of value added to employee compensation than goods-producing industries do. Spending did not merely migrate. It migrated toward sectors where more of each dollar ends up in someone’s paycheck.

So yes, one could argue that this still resembles the horse story in one respect. The relative importance of goods production declined as productivity increased. The point, though, is that large, diverse economies contain adjustment margins that horses never had. There are escape valves.

Comparative advantage keeps reappearing. When automation makes some activities extremely cheap, spending tends to shift toward the activities that remain relatively expensive. And the activities that remain expensive are often the ones that are hardest to automate. Those are precisely the areas where humans continue to hold a comparative advantage—that is, where human labor remains relatively more productive or valuable than machine substitutes. The saved dollar therefore tends to drift toward areas where humans are still worth paying.

That is not technological optimism. It is simply the logic of comparative advantage.

James Bessen documents this dynamic sector by sector. In early textile manufacturing, power looms sharply reduced labor required per yard of cloth. But cloth became so much cheaper that demand exploded, and total textile employment increased for decades. Similar patterns appeared in steel and automobile production. Eventually, demand saturated. Prices stopped falling rapidly enough to offset labor-saving automation, and employment in those sectors declined.

The key question for AI, then, is not whether automation can destroy jobs. Of course it can. The real question is: Which sectors are in which phase? Where might AI-generated savings flow today?

Health care already accounts for roughly 18% of U.S. GDP, and that share continues to rise. Elder care will likely expand further as populations age. Personalized services, human-intensive care work, and new categories of consumption may absorb growing shares of spending.

Joel Mokyr, Chris Vickers, and Nicolas Ziebarth make this historical argument well in a Journal of Economic Perspectivesarticle. Across prior waves of technological change, new tasks emerged, comparative advantage persisted, and entirely new categories of work appeared that earlier generations could not have anticipated.

Horses had no equivalent adjustment path. They did not move into elder care.

Will Humans Become a Luxury Good?

The saved dollar migrated toward human-intensive sectors last time. The strongest argument for why this time could be different comes from economist Philip Trammell’s paper, “Is Labor a Luxury in the Long Run?”

His answer is: probably not. Even if richer consumers initially spend more on human-intensive goods and services—live music, handmade products, personal care, bespoke experiences—four long-run forces may steadily erode that demand.

AI-generated variety keeps expanding. New AI-produced goods compete for every dollar that might otherwise land on a human-made product or service.

Human experiences carry opportunity costs. Time spent at a live concert is time not spent consuming some potentially superior AI-generated alternative.

Labor competes with other scarce goods for consumers’ willingness-to-pay premiums. Beachfront property, status goods, intellectual property, and research-intensive products may all absorb spending that might otherwise flow toward human labor.

Capital goods become cheaper over time. If investment opportunities continue expanding, the share of economic activity devoted to capital accumulation could grow indefinitely.

Trammell’s Coca-Cola analogy captures the intuition cleanly. Original Coke once held roughly 50% of the soda market. Then came Diet Coke, Cherry Coke, Pepsi Max, energy drinks, flavored sparkling water, and endless other varieties. Even with enormous brand loyalty and supply constraints, Coke’s market share fell below 20%.

The implication for AI is straightforward. Even if consumers initially prefer human-made goods, that preference may weaken as AI continuously generates new substitutes and varieties. Human labor does not need to become worthless. Its share can erode through dilution.

That is a serious argument, and I take it seriously. Still, notice what the argument requires. It is not enough for AI-generated variety merely to expand. That will almost certainly happen. The stronger claim is that AI-generated substitutes must expand broadly and rapidly enough to pull spending away from every human-intensive category simultaneously.

The real question is not whether AI competes with some human-produced goods. Of course it will. The question is whether any human-intensive islands survive. Does anyone still spend money on something with a person inside it?

The arithmetic quickly becomes more demanding than many “humans become horses” narratives imply. Suppose AI eventually captures 85% of economic activity. Software, accounting, logistics, medicine, law, management, and much of media production become almost fully automated. Human labor largely disappears from those sectors.

Now suppose the remaining 15% of spending flows toward activities that still contain at least 30% human labor: elder care, live entertainment, skilled trades, therapy, surgery, in-person education, luxury craftsmanship, status goods, and other relational or trust-intensive services.

The aggregate labor share would still equal at least:

S ? 0.15 × 0.30 = 0.045

That leaves labor with at least a 4.5% share of economic output. That may not sound comforting, but remember what this calculation is doing. It is merely establishing a lower bound under extremely aggressive automation assumptions. It is not utopia. It is not full employment. But it is also not zero. And a falling labor share does not necessarily imply falling labor demand if total output grows rapidly enough.

Alex Imas offers another reason to doubt the “humans disappear” story. As AI drives down the cost of commodities, real incomes rise. Historically, richer consumers tend to shift spending toward what Imas calls “relational goods”—goods and services whose value depends partly on human connection, scarcity, or social meaning.

That idea connects to a large economics literature on structural change. Over time, economies tend to shift from agriculture to manufacturing to services as incomes rise. The key debate is why. Do consumers simply buy more of whatever becomes cheaper? Or do rising incomes fundamentally change what people want?

Diego Comin, Danial Lashkari, and Marti Mestieri decompose those effects and conclude that income effects account for more than 75% of the long-run shift toward services. That distinction matters enormously here. If structural change were driven mainly by falling prices, then AI-generated abundance might pull spending overwhelmingly toward AI-produced goods. But if structural change is driven mainly by rising incomes and evolving preferences, then richer consumers may continue demanding more human-intensive experiences and services. Historically, that is exactly what has happened.

Experimental evidence points the same way. In one set of experiments, subjects learned that other people would be excluded from purchasing an otherwise identical product. Willingness to pay roughly doubled. The exclusivity itself created value.

Importantly, the exclusivity premium was stronger for human-made goods than AI-generated ones. Human-created artwork gained roughly 44% in value from exclusivity, compared with about 21% for AI-generated artwork. AI-made goods feel infinitely replicable. Human-made goods feel scarce, even when they technically are not. People value what other people cannot easily obtain. That impulse does not disappear as societies grow wealthier. If anything, it intensifies.

Perhaps AI-generated variety eventually overwhelms even those preferences. Maybe. Still, the structural-change evidence consistently suggests that income effects dominate price effects by roughly three to one. When basic goods become cheaper, humans do not announce that they are finally satisfied and stop developing new wants. They invent new forms of distinction, identity, taste, and status competition. The open question is where those new desires land. So far, the evidence points toward humans retaining an important role.

One final clarification matters here, because popular AI discussions often conflate two distinct claims. A falling labor share is not the same thing as falling labor demand. Labor’s share of national income can decline even while total employment and total wages continue rising, provided the overall economy grows fast enough. In that world, AI appears to “take over” a larger share of production while human workers still earn more in absolute terms because the economic pie itself expands dramatically.

That may well describe the phase we are currently entering. We already observe the basic pattern. Higher-income households consume more services, and service sectors remain relatively labor-intensive. Could that eventually reverse? Of course. But at the moment, this is the evidence we actually have.

The Horse Story Ends Here

Walking through all these layers—from tasks, where we are only beginning to see meaningful substitution, up through firms, sectors, and the macroeconomy—leaves me fairly skeptical of the “humans become horses” outcome. I know I have concealed that conclusion masterfully until now.

AI will absolutely perform many tasks. It will reorganize jobs, sometimes painfully. Some sectors may lose most of their human labor. Spending will often chase automation and lower prices. All of that can happen without driving human labor demand to zero. Because at every stage of the process, there is still a saved dollar looking for somewhere to land. And the same question keeps reappearing: Where does it go next?

For the horse outcome to occur, that saved dollar must eventually fail to find any activity with meaningful human labor embodied in it. Not some activities. All activities.

That is a very specific future. It is logically possible. But it requires substitution to dominate simultaneously across tasks, firms, sectors, and final consumption patterns, with no surviving human-intensive islands anywhere in the economy. The evidence we currently have—structural change, revealed preferences, comparative advantage, and experimental results—keeps pointing the other way.

Horses lost because the economy stopped needing horsepower. Humans are not just horsepower.

To provide the best experiences, we use technologies like cookies to store and/or access device information. Consenting to these technologies will allow us to process data such as browsing behavior or unique IDs on this site. Not consenting or withdrawing consent, may adversely affect certain features and functions.

Functional

Always active

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.