Kevin Warsh’s first press conference as Fed chairman was far better than I expected.

The statement is shorter, forward guidance is gone, and the Committee has promised to deliver price stability. That is most of the prescription I have made for at least fifteen years. But the question that actually matters – what the Fed should be trying to deliver, and the wreck of a regime Powell has left him – is still open.

Kevin Warsh held his first press conference as chairman of the Federal Reserve yesterday, and it was immediately clear that he has put himself firmly in the driver’s seat.

The statement was unlike anything Jerome Powell ever signed off on. It was substantially shorter. It dropped the elaborate “forward guidance” that had been the house style of the Fed for the better part of two decades. And in its place came a single, blunt sentence: “The Committee will deliver price stability.”

I have to admit I did not expect to be impressed. I have been a sceptic of Warsh for months, and I have said so in writing. So before I explain why he changed my mind, let me explain why I doubted him.

Why I Was Sceptical

Warsh did not look, until yesterday, like a man who would face down the White House and put the Fed’s credibility first.

He spent last year campaigning for the job, and he campaigned by telling the White House what it wanted to hear. He was outspoken in favour of lower rates, exactly as Trump has been demanding, and he justified it with the claim that an AI-driven productivity boom would expand supply and pull inflation down on its own.

That argument never persuaded me, and not because I doubt what AI might do to productivity. My objection is more basic. A productivity boom is a positive supply shock, and a central bank should not be reacting to supply shocks at all, positive or negative. If AI does raise productivity, the right response is to hold nominal spending on its path and let the gain come through as lower inflation and faster real growth. Cutting rates because supply is improving is using a supply-side story to justify a demand-side easing – exactly the confusion a rule-based Fed exists to remove.

There was also the question of qualifications. Warsh was a Fed governor from 2006 to 2011, the youngest ever appointed, but his record on inflation forecasting in those years was weak, and prominent NGDP advocates, Scott Sumner among them, were openly sceptical that he was the right man. As was I at the time.

And there was the politics. His IMF speech last April read, frankly, like a job application written for Trump’s ear – a list of grievances about institutional drift, wrapped in language about independence that pointed towards less of it rather than more.

There is, too, the family dimension, which under normal circumstances I would ignore entirely. Warsh is married to Jane Lauder, daughter of Ronald Lauder, a long-standing personal friend of Donald Trump.

These are not normal circumstances. The President has spent a year demanding lower rates and used a renovation investigation as a pressure tactic against Powell. When his preferred candidate to replace the chair turns out to be connected to his inner circle by marriage, that belongs on the analytical record.

There is one side of Warsh’s thinking I have always had sympathy for. He has been a consistent critic of the Fed’s mission creep into financial-stability and macroprudential territory. Those are my positions too.

But in May, on the day Powell chaired his final meeting, my complaint was precise: Warsh was full of diagnosis and empty of framework. He knew what he wanted to remove. He had said nothing about what would replace it.

So that was where I stood. Sceptical, unconvinced by the AI story, worried he would be Trump’s man, and waiting to see whether he had a regime in mind or only a grievance.

He did better than that. And that is why I am writing this.

Letting the Market Do the Work

The first thing you notice about Warsh’s statement is the length. It is substantially shorter than anything Powell put out. That is not cosmetic. The old statement told you what the Committee thought, how it read the data, and where it expected to move. The new one gives the target range, reaffirms ample reserves, notes inflation is still above 2%, and states – flatly – that the Committee will deliver price stability.

Warsh described it himself with understatement: a bit shorter, a bit simpler, dispensing with some older language. Gone, in particular, is forward guidance. And he declined to submit his own dot to the projections, on the grounds that a published rate path locks the central bank into a promise it cannot keep.

Clearly, this is the right instinct. So let me give it a name.

Years ago I defined the Chuck Norris effect like this: you do not have to print more money to ease policy if you are a credible central bank with a credible target.

The point generalises. A credible central bank does not have to do very much, because the market does the work for it. If everyone believes the Fed will deliver, expectations adjust on their own, and the threat to act is usually enough.

Warsh has not announced a rule. But by stripping the statement to a commitment and refusing to spell out a path, he is telling markets to read his reaction function rather than his quarterly mood. He is asking the market to do the lifting.

In its purest form, a fully credible Fed would hardly need to hold a press conference at all. It would be enough to say, once and for all: we will always, at any time, do exactly what is needed to deliver price stability.

The market does the rest. It is the market that implements the policy, and it is the market that makes the real forecasts, through its expectations.

The comparison that comes most naturally to me is not American. It is Danish. Denmark, where I live, runs a fixed-exchange-rate policy against the euro. The Danish central bank – Danmarks Nationalbank – publishes no elaborate forecasts and no guidance. It does not need to.

Everyone knows it will do whatever it takes to hold the krone fixed against the euro. That credibility is the policy, and the market enforces it. Warsh is now saying something structurally identical: we will deliver price stability, you do not need our forecasts, you need only believe us.

Contrast the opposite approach. For years the ECB under Mario Draghi, and Jean-Claude Trichet before him, insisted it would “never pre-commit” to any future action. I always thought that was precisely the problem. A central bank that refuses to say what it is trying to achieve forces the market to guess, and guessing is not a credible target.

Mission Creep and the End of Fine-Tuning

This is also the most refreshing thing about Warsh’s debut, and it goes beyond the statement. The Fed has spent the better part of fifteen years trying to do too much.

Since 2008 it has drifted into questions that have nothing to do with its mandate – financial-stability ambitions, distributional concerns, even climate-related risk. The mandate is price stability and maximum employment. It is not the management of every problem that happens to be fashionable.

So the narrowing Warsh implies is welcome.

There is an old principle, associated with Jan Tinbergen, that each policy target needs its own instrument; a central bank chasing five objectives with one rate will fail at most of them. Goodhart’s Law adds the rest: when a measure becomes a target, it stops being a good measure – which is exactly the trap macroprudential policy walks into.

Warsh, to his credit, seems to grasp both. The Fed has one instrument and should pursue one nominal objective. Everything else is someone else’s job.

This is, fundamentally, an argument about rules versus discretion. The Great Recession and its aftermath were an exercise in central-bank discretion – improvisation dressed up as sophistication. I have always thought we should go the other way, towards a Fed that behaves automatically, like the computer Milton Friedman wanted to run monetary policy. All central banks need to do this.

A Fed that fine-tunes is a Fed that surprises. A Fed that follows a rule is a Fed the market can anticipate. And a Fed the market can anticipate barely has to act at all.

Nominal Stability, Not Price Stability

But a great deal is still missing, and Warsh knows it. Which instruments should the Fed actually use – the money base, or the policy rate? Which measure of inflation is the right one? Should there even be an inflation target at all? My own answer, and my favourite, is a target for nominal GDP. So this is where my renewed optimism meets the hard question. Clarity is worth little if the target is wrong.

Warsh committed the Committee to price stability, which the Fed reads as 2% inflation. Notice what the statement leaves out. The mandate is dual – stable prices and maximum employment – and the new statement mentions only the first. It is a price-stability statement, not a dual-mandate one.

And here I would go further than Warsh did. He committed to price stability. I would commit to nominal stability instead, and the two are not the same thing.

Nominal stability – a stable path for total nominal spending – delivers price stability over time. Price stability pursued directly does not necessarily deliver nominal stability at any given moment. You can hold prices down in the short run by letting nominal spending collapse, or by tightening into a supply shock. That is not stability. It is the opposite, dressed up as discipline.

So it is not really prices a central bank should stabilise. It is nominal spending. Get the nominal path right, and prices look after themselves over the medium term.

My answer to the target question has not changed for more than fifteen years.

The Fed should target the level of nominal GDP – a 4% path, consistent with 2% inflation and around 2% trend real growth. It has two advantages over an inflation target, and both bite right now.

First, it handles supply shocks: a level target lets inflation rise temporarily after an energy shock while holding nominal spending on its path, instead of tightening into it the way the ECB infamously did in 2011.

Second, it makes up for past misses. An inflation target lets bygones be bygones; a level target claws the overshoot back. That is the difference between an anchor that holds and one that drifts.

Now look at what Warsh is staring at. Consumer price inflation hit 4.2% in May, the highest in three years. Producer prices ran above 6%. The Iran war drove oil from around $67 in late February to an intraday peak near $119 in March. The Committee’s median projection now has the policy rate ending the year at 3.8%, a quarter point above today, where three months ago it expected a cut.

So the dot plot has flipped from a cut to a hike, and it is hard to read Warsh’s debut as anything other than a hike now being more likely than a cut.

Here is the part most commentators will miss. The current inflation has two sources, not one. Part of it is the energy supply shock – and a central bank should look through that, not tighten into it.

But part of it is excess nominal demand the Fed never wound back – nominal spending that has run above trend since 2021 and is still drifting higher, as I will show in a moment. A pure inflation-targeter cannot tell the two apart and risks getting both wrong. A nominal GDP target separates them automatically – look through the oil, lean against the excess nominal demand. It is the one framework that gets this moment right.

This, by the way, is why the whole “hawk versus dove” framing is, frankly, useless. To be hawkish or dovish is already to assume policy should be set by someone’s discretionary feel.

What should concern us is not the temperature of the chairman. It is the regime.

The Five Task Forces

In May my complaint was that Warsh offered no framework. Yesterday he began building one, or at least the machinery to build one.

He announced five task forces, each on a core area of policy: communications, the balance sheet, data and data sources, productivity and jobs in an era of transformation including AI, and inflation frameworks examined from first principles.

Each one, Warsh said, would draw on the best minds inside and outside the economics profession, backed by Fed staff, and report to the policymakers.

Two things stood out by their absence. There was no hint – none – of the easiest dovish escape available to him: quietly raising the inflation target, or hiding behind its “flexible average” wording, to make five years of overshoot vanish on paper.

He could have conjured the problem away. He chose not to. And he barely mentioned AI, even though it has a task force of its own. The man who last year leaned on an AI productivity boom to justify the rate cuts Trump wanted did not reach for that argument once.

Which leaves the question I keep coming back to: who. If the inflation-frameworks task force is serious about first principles, the names I would want in the room are obvious – Scott Sumner, David Beckworth, Peter Ireland, and Josh Hendrickson on nominal GDP and policy rules; George Selgin on the balance sheet, where the ample-reserves regime is his territory; and, for any of it, my friend Bob Hetzel, the finest monetary historian the Fed has produced ever. Appoint people like that and “from first principles” might mean something. Appoint the usual committee and it will not.

What I Have Proposed

So let me be concrete about what I would actually have the Fed do, because I am not asking the task force to invent anything. I wrote it down almost exactly ten years ago, in January 2016, and I would not change a word.

First, a 4% nominal GDP level target, defined on the expected level of NGDP eighteen to twenty-four months out. That one target delivers both price stability and maximum employment. No other is needed.

Second, the Fed should stop producing its own forecasts and instead read the market’s: a prediction market for NGDP twelve and twenty-four months ahead, the surveys of professional forecasters, and market-based models of NGDP expectations. Let the market tell the Fed where nominal spending is heading, not the other way round.

Third, give up interest-rate targeting – the dot plot included – and use the monetary base as the instrument. Announce a permanent base-growth rate set to hit the 4% path, justified by one number only: expected NGDP against the target. Leave interest rates entirely to the market.

The consequences follow directly.

The policy is rule-based, not discretionary. It is transparent, with the market doing most of the implementation – the Chuck Norris effect made operational.

There is no zero-lower-bound problem, because control of the base can ease even when interest rates sit at zero. The endless and, frankly, silly talk of bubbles, moral hazard, and macroprudential fine-tuning stops, because the Fed gives up pretending it can do a better job than the market in ‘forecasting’. The Fed stops reacting to supply shocks, positive and negative. And the FOMC could, at last, be handed to the computer Milton Friedman wanted to run it.

I called it, at the time, a forward-looking McCallum rule. The label matters less than the shape of the thing: one target, read from the market, hit with one instrument, justified by one number.

Look at Warsh’s five task forces and you will see the same agenda, broken into committees – inflation frameworks is my first change, communications and data my second, the balance sheet my third. The only real question is whether they follow the framework to where it leads, or spend a year rediscovering why the Fed has always preferred its own discretion.

What He Inherited

All of which raises the obvious question. Why does any of this matter so much? Why is the regime question existential rather than academic?

The answer is the Fed that Warsh has inherited. Because it is not a healthy institution. It is a weakened one, and the weakness is to a large extent self-inflicted.

Trump has spent the past year arguing that Powell ran policy too tight. The data says the opposite.

By my reckoning, Powell ran the easiest monetary policy in modern Fed history, and the cleanest way to see it is not through inflation or the funds rate but through the level of nominal spending – nominal GDP.

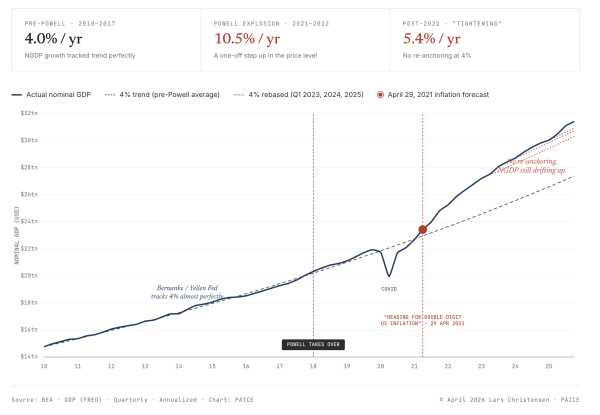

From 2010 through 2019, US nominal GDP grew at almost exactly 4% a year. That was the de facto regime under Ben Bernanke and Janet Yellen, broadly consistent with their stated 2% inflation goal given trend productivity and labour-force growth.

I have argued for years that this implicit anchor, and not the dual mandate the Fed talks about, was what actually held the system steady. The Covid shock knocked nominal spending below the path in 2020, and the Fed’s emergency response that spring was, in my view, exactly right.

Then came 2021.

On 29 April 2021, I published a post on this blog titled “Heading for double-digit US inflation.”

I argued that the explosion in US broad money, combined with the largest fiscal expansion since the Second World War, would produce a fast, large, one-off jump in the price level – and that what happened next would depend entirely on whether the Fed moved to anchor expectations or let its credibility erode.

The forecast was right. Headline CPI inflation peaked at 9.1% in June 2022, the highest in four decades. The point is not that I got it right. The point is that the call was available to anyone willing to read the data.

The broad-money numbers were public. The fiscal arithmetic was public. The lags between money and inflation that Milton Friedman identified decades ago are textbook material.

And the Fed, under Powell, chose to do nothing.

Worse than nothing. In 2020 the FOMC had adopted Flexible Average Inflation Targeting, which committed it to running inflation above 2% for a while after running it below. Defensible in theory. A catastrophe in practice.

Through 2021 and into 2022 the Fed held the funds rate at zero and kept buying $120 billion of assets a month while nominal GDP grew 11% in 2021 and close to 10% in 2022 – more than two and a half times the established 4% rate. That is not flexible average inflation targeting. It is the monetary equivalent of price-fixing, and all the while the Fed insisted the inflation was transitory, a word it kept using long after the indicators had made it indefensible. This was not a close call.

Powell then spent 2022 and 2023 cleaning up the mess, and he deserves credit for it. From near-zero in March 2022 the Fed reached 5.25-5.50% by July 2023. Inflation came down, the labour market did not collapse, and that successful disinflation is the one thing from the Powell era I will give him unambiguous credit for.

But the disinflation did not restore the regime. The price-level jump is permanent – undoing it would take a Volcker-scale recession, and with federal debt above 100% of GDP and interest payments above $1 trillion a year, that is no longer arithmetically possible without risking a sovereign default.

The growth rate, though, is a separate matter. Having allowed the one-off jump, the Fed could at least have re-anchored nominal spending at 4% from there. It did not. On my numbers, NGDP growth has averaged about 5.4% a year since the start of 2023, and from the start of 2025 it has run above 6%. The rate is drifting up, not settling.

So the Fed of 2025 and 2026 is not running a tight policy that has restored discipline. It is running a policy that still accommodates above trend. The “tightening” belongs in scare quotes: it is tight relative to the Fed’s own 2021 error, not relative to any credible framework. This is the excess nominal demand I pointed to earlier. The Fed is still too easy.

Why the Attack Lands

So why, if Powell ran the easiest money in modern history, does Trump’s accusation that he was too tight gain any traction at all?

It lands because the Fed proved, in real time, that it cannot be trusted to act on the inflation indicators when its own framework tells it not to.

That is the credibility deficit Warsh inherits, and it is worth more to Trump than any number. A Fed that had read the money data correctly in 2021 and headed off the inflation would now be defending its independence from overwhelming strength. Trump’s attacks would land in empty air. Instead the Fed defends independence from partial credibility, having handed the public a 9% inflation to absorb. The easy money of 2021 and the political crisis of 2025-26 are not two stories. They are one.

The historical rhyme is the early 1970s. Nixon leaned on Arthur Burns – the tapes record instructions, not requests, to expand the money supply before the 1972 election – and Burns complied, explaining at each meeting why the next move could wait. Each decision sounded reasonable on its own. The cumulative result was a decade of inflation and, eventually, a Volcker disinflation that drove unemployment towards 11%.

The parallel to Powell is only partial. He raised rates hard, the disinflation was real, and he resisted Trump’s public pressure throughout. On the political dimension he was not Burns – or rather at least not quite as bad a Burns.

But on the analytical dimension – the willingness to ignore the monetary indicators because the prevailing framework said they did not matter – the parallel is uncomfortably close. Burns ignored the aggregates because his framework dismissed them. Powell ignored them in 2021 because FAIT said the inflation was wanted. The justification differs. The shape of the failure is identical.

And underneath all of it sits the deeper threat: fiscal dominance.

Federal debt held by the public is above 100% of GDP in the US.

Net interest has gone from around $350 billion in 2020 to over $1 trillion in 2025. Every 100 basis points on the policy rate eventually adds about 1% of GDP to the interest bill. The federal government now has a powerful, mechanical reason to want low rates regardless of what the macroeconomy needs – and Trump has been unusually explicit that he wants rates down for the budget.

That is fiscal dominance: the fiscal authority’s needs crowding out the central bank’s independence. It is the condition behind nearly every serious inflation in history, from the German hyperinflation of 1923 to the post-Soviet Russian inflation, chronic Argentine inflation, and the Turkish episode under Erdoğan.

Not Trump’s Fed Chairman

So set Warsh’s debut against all of that, and the most important thing he did yesterday is the thing I least expected. He defied the White House.

Trump appointed him after attacking Powell for not cutting, and Warsh had spent the previous year signalling sympathy for exactly those cuts.

The natural bet was that he would ease, or at least signal easing – the cuts the President wanted. Instead he held rates on a unanimous vote, let the dots tilt towards a hike, and gave a press conference the markets took as anything but the relief Trump was hoping for.

The S&P 500 fell. Bond yields jumped. Asked whether he had spoken to the President since taking the job, he said only: “I don’t have anything for you.” He has a mandate, and he intends to deliver on it. Whatever Trump says.

Set that against everything stacked the other way – the campaign for lower rates, the IMF speech, the Lauder connection, and the fiscal-dominance pressure that gives any modern president a mechanical hunger for cheap money. On his first day, with all of that pushing one way, Warsh pushed back. This is the Arthur Burns fear answered, at least for one meeting.

And there is a deeper point underneath it. The more rule-based and automatic policy becomes, the less it matters who the chairman is, and the less influence any president has over him. A discretionary Fed can be lobbied, pressured, and bullied. A rule-based Fed cannot.

Taking discretion out of monetary policy is not only better economics. It is the strongest protection of central bank independence there is – which, with fiscal dominance bearing down on the Fed, is no small thing.

Warsh also made a point of noting that inflation has now run above the 2% goal for more than five years. He inherits that overshoot, the same five years and the same failure. If he means what he says, it has to end. A central bank that overshoots for five years and shrugs has no credibility, and without credibility none of this machinery works.

The Hard Part Has Started

So I come away more optimistic than I expected, and far more than I was a month ago. The communication is sharper. The mission creep is being reversed. He defied Trump on day one. And the instinct – say what you will deliver, then let the market do the work – is exactly right.

But the easy part is the part Warsh has done. Shortening a statement, dropping a forecast, and holding the line against Trump for one meeting is style and nerve. Choosing the right thing to be clear about is analysis, and it is unresolved.

Friedman taught that monetary policy works with long and variable lags and cannot fine-tune the economy. Scott Sumner updated it: long and variable leads, because the work runs through expectations. Both point to the same conclusion. What matters is the regime, not the meeting-to-meeting decisions. A Fed that spent five years being careful about each meeting lost the regime entirely – and that, not any single rate call, is what Powell leaves behind.

So it was never really a rate decision. It is a regime decision. Warsh has made a good start on the things that are mostly nerve. The thing that is analysis – whether the Committee anchors on nominal spending or on an inflation number that has already failed for five years – is still to come. And in practice, reading all of this together, it is hard not to see a rate hike now as more likely than a cut.

The chairman changed in May. The hard part started yesterday.

Related

Nicole Byers is an entertainment enthusiast! Nicole is an entertainment journalist for the Maple Grove Report.