Hong Kong – Fairmont Hotels & Resorts, the globally renowned luxury hospitality brand, today introduces “Wellness Without Walls,” an innovative worldwide campaign that expands the concept of well-being beyond the traditional boundaries of a gym or spa. This campaign features Kylian Mbappé, the internationally celebrated football superstar, as Fairmont’s inaugural Wellness Ambassador. The campaign includes a cinematic brand film that vividly brings this limitless vision to life, captured through the perspective of one of the world’s most recognizable athletes. Mbappé’s personal approach to performance, recovery, and longevity reflects and embodies Fairmont’s deep-rooted philosophy of holistic well-being.

Fairmont La Hacienda Hotel golf course and view to Gibraltar, La Alcaidesa, Andalucia. Spain

“Fairmont offers an authentic commitment to wellness in each of its locations, which is why I am eager to partner with them,” said Kylian Mbappé. “As an athlete, recovery and balance are crucial, and I experience this commitment during every stay. With Fairmont, it’s possible to maintain your routine – even when traveling – without feeling forced.”

world-renowned footballer Kylian Mbappé as Fairmont’s first-ever Wellness Ambassador

The brand’s new philosophy, expressed through the campaign, emphasizes that wellness should be accessible, relevant, and integrated into everyone’s life. In addition to the new premium Nike gear lending program, Fairmont provides travelers with a wide range of well-being experiences, all while celebrating the amazing destinations, cultures, and communities where they are located.

Fairmont Wellness Campaign

Claudia Kozma Kaplan, Chief Brand Officer, Fairmont Hotels & Resorts, said, “Fairmont is thrilled to partner with Kylian Mbappé as the brand embarks on a systemic shift on how it delivers wellness. Today’s luxury hotel guests are increasingly more aware of how they feel, how they perform, and how they recover. They are not always looking for high intensity or prescriptive programs, but for experiences that help them stay well and make better use of their time. The new campaign’s ‘No Excuses’ tagline is inspired by Fairmont’s promise that guests can effortlessly maintain their well-being routine while traveling, however they personally define it, be it for a guest with the discipline of an elite-athlete or someone who prefers a more leisurely amble by bicycle with friends.”

Fairmont, a distinguished participating brand within the comprehensive portfolio of ALL Accor, brings this innovative wellness concept to life through an extensive, thoughtfully curated collection of experiences, services, and touchpoints. These offerings are designed to immerse guests in a seamless, holistic well-being journey from the moment they arrive at the properties. Guests can indulge in a variety of unique activities, including cold immersion therapy at the luxurious Fairmont Chateau Lake Louise, where they can rejuvenate in crisp, icy waters surrounded by stunning mountain scenery; engage in forest therapy at Fairmont Jasper Park Lodge through guided walks and mindfulness exercises; enjoy hydrotherapy sessions at Fairmont La Hacienda on Costa del Sol, with expertly designed treatments in serene, spa-like settings; try paddleboarding on the calm waters near Fairmont Austin for a blend of exercise and relaxation; participate in copal cleansing rituals at Fairmont Mayakoba to rejuvenate the spirit and body; engage in friendly matches of badminton or cricket at the historic Fairmont Udaipur Palace, blending sport and cultural immersion; and finally, indulge in an elevated bathhouse experience at Fairmont Hanoi, featuring traditional and modern therapies to relax and detoxify. Each of these specialized offerings creates an immersive environment that promotes wellness, relaxation, and mindfulness, making every guest’s experience unique and enriching.

Fairmont Chateau Lake Louise

Emma Darby, Global Vice President Spa & Wellness, Fairmont Hotels & Resorts adds, “Travel is no longer just a break. It is an opportunity to maintain rhythm, restore balance, and experience something that supports how our guests live. The world does not need more wellness spaces, it needs more space to be well. This coupled with experiences that only Fairmont can deliver, is redefining what wellness at Fairmont truly means.”

“Wellness Without Walls” symbolizes Fairmont’s ongoing dedication to enhancing wellness throughout its worldwide locations. The brand will expand and refine its services by launching new experiences, forming partnerships, and promoting the philosophy that every guest should feel their best, no matter where they are.

Here’s a number that should stop you mid-scroll: India’s gross NPA ratio hit a historic low of 2.15% as of September 2025 — the lowest level since 2010-11, confirmed by the RBI in its latest Trends and Progress of Banking in India report released December 2025.

Now here’s the number that puts it in context: the absolute gross NPA stock still stood at ₹4.32 lakh crore.

That gap — between a ratio that looks reassuring and an absolute number that demands serious infrastructure — is exactly where India’s debt collection industry lives in 2026. The headline is good. The operational challenge is not over. And the technology being deployed to close that gap is transforming the industry faster than most lenders have internalized.

Understanding India’s NPA story in 2026 requires holding two truths at once.

The first truth: asset quality has genuinely improved. Public sector banks saw their gross NPA ratio fall from 9.11% in March 2021 to 2.58% by March 2025. Net NPAs are at 0.5%. The slippage ratio — which measures fresh loans turning bad — declined for the fifth consecutive year to 1.4% at end-March 2025. By almost every ratio-based metric, this is the healthiest India’s banking sector has been in a generation.

The second truth: the composition of what’s left has changed dramatically. The easy-to-resolve large corporate NPAs have largely been worked through the IBC pipeline. By March 2025, more than 30,000 applications representing underlying defaults of ₹13.78 lakh crore had been settled at the pre-admission stage alone. What remains is a harder, more distributed problem — retail loans, MSME advances, microfinance accounts, scattered across geographies, ticket sizes, and legal jurisdictions. India’s loan book crossed ₹2.2 trillion in FY25, with personal loans alone doubling from 73 million to 146 million accounts in three years.

More loans at smaller ticket sizes, more borrowers who are first-time credit users, more accounts that fall into DPD buckets without the ability to recover through traditional legal channels. The ratio looks good. The recovery work is just beginning.

Technology Has Stopped Being Optional

If 2023 was when collections technology became mainstream, 2026 is when it became existential. The proof is in the adoption curves.

Mid-sized banks observed a 34–36% drop in credit disbursement and collection costs due to AI adoption. Institutions implementing AI-driven collections strategies report recovery rate improvements of 10–25% and significant reductions in operational costs. AI adoption in finance functions has climbed to 59% of firms globally — up from just 37% in 2023.

In India specifically, the pattern is clear: platforms that started with digital nudges and payment reminders have graduated into full-stack recovery infrastructure. Credgenics, which recently partnered with Aye Finance, now combines omnichannel communication with AI-powered borrower scoring, a litigation management system, and an ODR capability — covering the collections lifecycle from the first payment reminder to settlement. DPDZero has built intelligent early-stage workflow automation with strong pre-legal capabilities. Both represent real progress on the front end of the collections funnel.

Industry leaders entering 2026 are clear that AI will act as a major catalyst across servicing, collections, underwriting support, and operational efficiency — with customer-facing adoption following with the right regulatory safeguards in place.

But here is where the story gets more nuanced: most of the AI investment in Indian collections has been concentrated in the 0–90 DPD bucket. The pre-legal stage. The moment a borrower crosses into formal legal territory — a SARFAESI notice, a DRT filing, a Section 138 cheque bounce case — the sophistication level drops sharply. Legal recovery in 2026 is still largely manual at most lenders, tracked through spreadsheets, coordinated over WhatsApp, and measured through gut feel rather than data.

This is the infrastructure gap that defines the next wave of collections technology in India.

Where The Legal Stack Is Breaking

Legal recovery was never meant to be the last resort. Under SARFAESI, lenders have the right to take possession of secured assets without court intervention. Under the IBC, creditors have genuine leverage. Debt Recovery Tribunals were specifically designed to fast-track financial disputes.

The frameworks work. The execution doesn’t — not at scale.

Consider what a legal recovery workflow typically looks like at a mid-sized NBFC with 5,000 NPA accounts: notices are drafted in batches, manually checked, dispatched through India Post without systematic delivery tracking. Court hearing dates live in someone’s calendar. Advocate assignments are based on familiarity rather than performance data. If a case gets adjourned three consecutive times with no action, there’s often no automated alert. The account drifts.

Over 320 new debt recovery platforms launched between 2022 and 2024 offering integrated dashboards, cloud-based workflows, and multilingual customer engagement. Yet very few of these have solved the legal layer — jurisdiction-specific notice templates that pull directly from loan management data, court case tracking that flags at-risk hearings, advocate performance analytics that tell you which empanelled lawyer closes DRT cases fastest in a specific geography.

Platforms built specifically for the collections-to-legal junction are filling this gap. Legodesk’s infrastructure, for instance, is purpose-built around exactly this workflow: legal notice automation with India Post integration and tracked delivery, centralized court case management across DRT, NCLT, and civil courts, and advocate network analytics that surface performance data rather than just contact information. The goal is to make the legal recovery process as operationally tight as pre-legal collections has become — auditability built in, data flowing both ways, outcomes measured.

The Regulatory Ratchet Is Only Moving One Way

The regulatory environment in 2026 is not getting simpler. The Digital Personal Data Protection Act, now operationalized through sector-specific guidelines from RBI, SEBI, and IRDAI, has fundamentally changed how lenders must architect their data flows, consent management, and vendor relationships. Regulation is emerging as a structural force rather than a cyclical hurdle for Indian fintechs entering 2026.

In collections specifically, this translates to: contact hour restrictions that require systematic enforcement, documentation requirements that demand automated audit trails, and borrower communication protocols that need to be embedded in the platform rather than left to individual agent discretion.

The lenders best positioned for this environment are the ones who treated compliance infrastructure as a capability investment rather than a cost center. Automated legal notice dispatch — where every notice is templated, timestamped, and tracked — is not just operationally efficient. It is legally defensible in a way that manual processes are not. When the RBI or a DRT asks for evidence of process, a documented digital trail answers that question in minutes. A WhatsApp archive does not.

The Emerging Recovery Ecosystem

One of the more interesting structural shifts in India’s collections space over the last 18 months is the move away from “one platform for everything” thinking toward ecosystem thinking.

Different parts of the recovery journey call for genuinely different capabilities. Pre-litigation resolution through platforms like Presolve360 is creating real value for smaller-ticket disputes — ODR and mediation reduce the burden on formal legal channels for accounts where SARFAESI or DRT proceedings would cost more than the debt itself. Early-stage collections automation from platforms like DPDZero works best when it’s connected to legal escalation triggers rather than operating as an isolated system. Legal management infrastructure like Provakil serves the enterprise legal function well, even where it isn’t collections-specific.

The lenders achieving the best recovery outcomes are not choosing between these. They are building recovery stacks — thinking clearly about what capability handles which stage of the journey, where data needs to flow between systems, and what the handoff protocol looks like when a borrower moves from pre-legal to legal territory.

This ecosystem mindset is relatively new in India. It is where the industry is headed in 2026, and the lenders who get there first are building a durable operational advantage.

What The Number Actually Tells You

Back to that opening statistic. A 2.15% NPA ratio is a genuine achievement — the result of eight years of sustained effort across regulatory reform, IBC implementation, recapitalization, and increasingly sophisticated recovery operations.

But ₹4.32 lakh crore in absolute gross NPAs, sitting in a loan book that is growing at double digits annually, with a retail and MSME composition that requires more distributed, technology-intensive recovery operations than anything India’s collections industry has managed before — that is not a problem that a good ratio solves.

It is a problem that infrastructure solves. And in 2026, the infrastructure is finally being built.

Legodesk provides legal recovery infrastructure for banks, NBFCs, and fintechs — connecting collections workflows with legal notice automation, court case management, and advocate network analytics. Contact us

FAQs

What is India’s current NPA ratio in 2026?

India’s gross NPA ratio reached a historic low of 2.15% as of September 2025, according to RBI data confirmed in February 2026. In absolute terms, gross NPAs stood at approximately ₹4.32 lakh crore as of the same period.

How is AI being used in debt collection in India?

AI is being deployed across predictive default scoring, omnichannel borrower communication, automated legal notice dispatch, and court case management. Mid-sized banks have reported a 34–36% reduction in collection costs after AI adoption, with recovery rate improvements of 10–25%.

What laws govern debt recovery in India?

How is AI being used in debt collection in India? A: AI is being deployed across predictive default scoring, omnichannel borrower communication, automated legal notice dispatch, and court case management. Mid-sized banks have rep

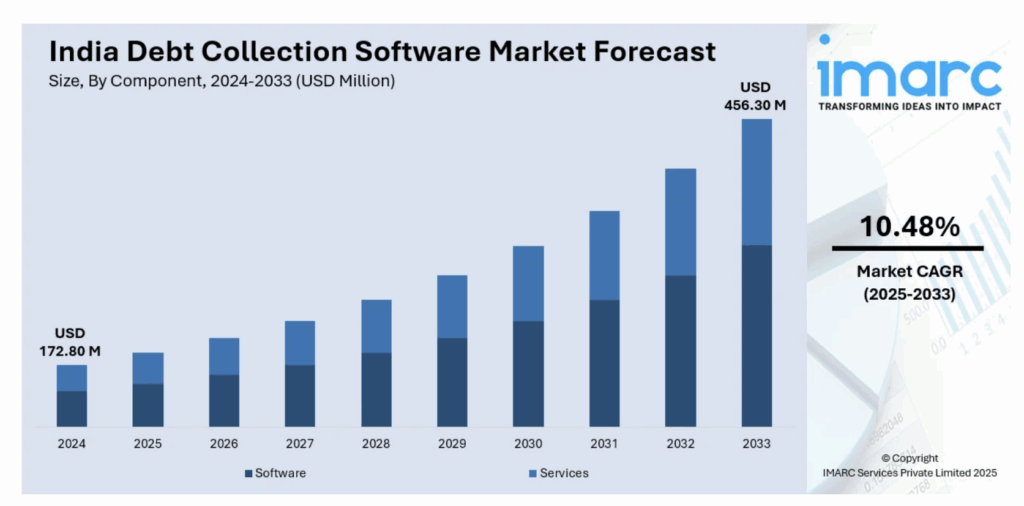

What is the size of the debt collection software market in India?

India’s debt collection software market reached approximately $172.8 million in 2024 and is projected to grow to $456 million by 2033 at a CAGR of 10.48%, per IMARC Group.

To provide the best experiences, we use technologies like cookies to store and/or access device information. Consenting to these technologies will allow us to process data such as browsing behavior or unique IDs on this site. Not consenting or withdrawing consent, may adversely affect certain features and functions.

Functional

Always active

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.