We may receive a commission on purchases made from links.

Automobiles have come a long way since the days of the Benz Patent Motorwagen, and so has the tech that powers them. Through the years, automakers have dedicated themselves to creating safer designs and comfort features that make driving a pleasure. But manufacturers can only do so much. When you still don’t have everything you want in a driving experience, it’s time to turn to aftermarket products.

A quick glance at Amazon’s automotive section gives you inspiration you didn’t know you were looking for. You can buy just about anything these days to upgrade your car, inside and out. From lighting and cameras to conveniences like extra cooling and in-car refrigeration, you might be surprised at the things you can add to your vehicle. We explored what’s new in the Amazon automotive category and found quite a few worth checking out. Here are the 10 that stood out the most based on usefulness and uniqueness.

Vantrue New N4S 3 Channel Dash Cam

Believe it or not, dash cams are good for more than just making social media videos. For starters, footage can be valuable if you’re ever in an accident. They may also help deter theft, and some can even document what’s happening in front of your car when you’re parked. Vantrue’s new N4S 3-channel dash cam is one example. Despite being in Amazon’s New in Automotive category, it’s already earned a 4.4-star rating from more than 240 reviews.

The Vantrue N4S camera offers 360-degree views and works under dark or low-light conditions and in high-heat situations. It records in HD to enhance small details like license plate numbers. It uses a magnetic GPS mounting system that doesn’t require wires or tools, so anyone can use it in any vehicle. There’s also a parking mode that will record events when it detects motion. To get your footage, you can download clips through the app via the camera’s built-in Wi-Fi or retrieve them from a microSD card. The Vantrue New N4S 3-channel camera is available on Amazon for $279.99.

Saker Car Vacuum Portable Cordless 20000Pa Suction Power 4 in 1

There’s no shortage of portable vacuum cleaners for the car on the market. But the Saker portable car vacuum is a little different. Most car vacuums excel at one job: vacuuming. And even then, they’re limited in where they can clean based on their size and attachments. The Saker car vacuum solves that issue with a variety of attachments suited for even the tiniest nooks and crannies of a vehicle. Precision tips can fit into small cracks and crevices, while a wide head can clean larger areas like seats and floorboards with fewer passes.

Along with its vacuuming capabilities, it can also function as an inflator, a vacuum sealer, and a blower. And unlike most other car vacuum cleaners, this one includes an LED screen that shows you things like wind power and battery levels. Its handheld design makes it small enough to store in a glove compartment or under the seat. It also uses a common USB-C connection, so you can charge the vacuum in your car, with a power bank or laptop, or using a separate power adapter. You can get the Saker 4-in-1 car vacuum on Amazon for $69.99.

NeaLia Wireless Magnetic Trailer Lights

If you choose to pull a trailer, that trailer needs lights. Aside from being the law, it’s common courtesy to your fellow drivers. And while most trailers come with built-in tail lights, those aren’t always enough. Whether your current tail lights are too dim or need to be replaced and you just don’t like dealing with wiring, these wireless magnetic stick-on trailer lights could be a possible solution.

NeaLia wireless magnetic trailer lights are exactly what they sound like: wireless lights that attach to a trailer or tailgate via magnets. Instead of hassling with a wiring harness, the lights use an external antenna and transmitter to activate the lights when you turn on the car, signal, or brake. Inside, the LED lights are bright enough to see under different lighting conditions. Since there’s no permanent installation required, you can switch the same set of lights between vehicles in seconds. One potential downside is that the lights have to be charged occasionally. Even with a 24-hour battery life, it might be good to get into the habit of recharging the lights after each use. You can get a set of two magnetic trailer lights on Amazon for $49.99.

Xool 3-Speed Car Fan for Backseat, Dual Head

Most new cars these days come with vents in the backseat so passengers can feel a cool blast of air as soon as you turn on the car. But this comfort feature still isn’t standard, and many older models don’t have backseat vents. One solution is to add a car cooling option, like a fan, and this 3-speed car fan from Xool looks pretty cool (no pun intended).

The car fan is made for backseat passengers. It attaches to the front seat headrest without being obtrusive. This one includes not one but two fan heads that can move independently of each other. You can point one at yourself and one at the person next to you, or keep both fans centered on you for extra cooling. Both fan heads are attached to a swivel-type arm that can move and fold to increase the fan’s cooling range. The fans can operate on one of three cooling settings and use a battery that you can recharge via your car or a portable power bank. You can get this car fan on Amazon for $19.99.

Manastin 12 Volt Car Refrigerator

Car fridges have grown in popularity over the years, and for good reason. They solve many of the downsides of traditional coolers and cost roughly the same. For starters, car refrigerators don’t require ice to keep your goods cold. No ice also means no mess. And some car fridges can even keep frozen items frozen for hours.

This car fridge from Manastin gives you two sizes to choose from: 37 quarts or 58 quarts. It looks about the same as a regular cooler in terms of style and size. The main difference is that it can reach temperatures of -4 degrees Fahrenheit and keep a consistent temperature for hours. If you’re grocery shopping in another town, you can fill the car fridge with meats or frozen goods and trust they’ll be just as fresh as the moment you bought them. This option also includes a dual-zone design so you can house different items at different temperatures. Use the app to control the temperature from your seat and check on battery level and cooling status. And since it’s made specifically for the car, you can power it via your car’s battery to ensure no gaps in cooling. The smaller version of the Manastin car refrigerator sells for $199.99 on Amazon, while the larger size is available for $234.99.

Rigstne Electric Cooler Bag

For some, a whole car fridge might be overkill, especially if you’re only carrying one-off items. Also, car fridges only cool or freeze, which doesn’t account for the other side of the food transportation spectrum. That’s why this electric cooler bag caught our attention. It warms and cools, plus it’s compact enough to fit in any backseat or trunk.

About the size of a small duffel bag, the electric cooler bag can reach temperatures as low as 46 degrees Fahrenheit or up to 140 degrees Fahrenheit. The bag itself weighs just 3.5 pounds, much lighter than a traditional cooler, yet it’s big enough to hold up to 20 canned drinks at a time. Similar to car fridges, you can power the electric cooler bag on the go via your car’s power outlet. It can serve as your heated lunch box on the go or as a mini cooler that doesn’t need ice. While it doesn’t have many reviews yet, some customers have mentioned it works well enough to keep drinks cool and doesn’t take up much space.

TruCozie Mattress Vacuum Cleaner with 275nm UV-C Light

Yes, the name says “mattress vacuum cleaner,” and the majority of people don’t keep mattresses in their cars. However, this versatile vacuum cleaner easily works on car seat upholstery. A handheld design makes it easy to sweep the device over the surface of your seats.

It goes beyond just sucking up dust and debris. A HEPA filter helps to trap allergens and small particles that many other car vacuums would leave behind. It includes built-in UV lighting, heat, and ultrasonic features to break down particles and pull them away. There’s also built-in aromatherapy to leave behind a fresh, clean scent, and anion technology to neutralize odors and reduce floating particles in the air. It’s made for mattresses but adapts well to the car. For many, cleaning the car means focusing on how it looks, and sanitization is usually forgotten. This handy vacuum can do both, and it’s available on Amazon for $99.99.

AeternaSol 200W Car Power Inverter 12V to 110V

Every car has some sort of power outlet so you can charge your devices or power electronics on the go. Most cars still have that “cigarette lighter” outlet style, which you might have thought was obsolete. More modern vehicles include USB-C outlets, which are ideal for charging cell phones and other electronics. Very few have a standard power outlet like what you’d find in your home. The AeternaSol 200W car power inverter can change that.

This power inverter is made to work with your car’s battery. It plugs into the cigarette-style outlet and gives you access to multiple outlet styles: two AC outlets, two fast-charging USB-C outlets, and two USB-A outlets. Ultimately, you can charge up to six different devices with this single power inverter. It also comes with an extra-long cable so you can share the charging ports with passengers in the backseat. Overall, the device is smaller than your smartphone and gives you more freedom than a standard automobile charging port. It’s available on Amazon for $21.99.

Thumok Magnetic RV Solar Lights Outdoor

Anytime you go camping, good lighting is a must. The problem is that most camping light options are made for one purpose or one use at a time (think flashlights, lanterns, headlamps, etc.). These magnetic RV solar lights change that. Use them in a pair to light up a large portion of your campsite, hands-free. They’re motion-sensing and will automatically turn on when you’re moving about the campsite, so you’ll always have lighting when you need it.

These magnetic solar lights are made for RVs, but given their design, you have more ways to use them. Their magnetic construction means all you have to do is stick them on your rig. There’s no hardwiring or permanent installation, so you can swap them between vehicles or other uses as you need. They run on solar power, so there’s no need to worry about recharging them when you’re on the go. You can get a set of two magnetic RV solar lights on Amazon for $24.99. They’re also available as a single light or in a pack of four.

Yakry Mini Car Air Ionizer

Your options for car air fresheners aren’t limited to DIY car fragrances or what you can hang on a rearview mirror, nor do you have to settle for artificial fragrances to make your car smell fresh. This mini car air ionizer offers a fragrance-free solution, which could be ideal for anyone with allergies or sensitivities to scents. Like some car air fresheners, this ionizer clips onto an air-conditioning vent. The difference is that it still allows air to flow through the vent instead of blocking it altogether.

While in use, the ionizer releases positive and negative ions to capture and reduce smells in your vehicle, like smoke, pet odors, and stale air. Instead of masking odors, which is the case for most sprays and air fresheners, this one neutralizes odors without using any type of fragrance. It’s also filterless, so once those smells are gone, they’re gone for good instead of being trapped in a filter you might not remember to change. You can get this mini air ionizer for the car on Amazon for $31.99.

How we chose these new pieces of automotive tech on Amazon

Choochart Choochaikupt/Getty Images

We had a few requirements for automotive tech to make it on the list. For starters, we only considered products that are readily available on Amazon. We only looked at products being sold by first-party brands, not third-party sellers. Next, each item had to be listed in the New Releases section in the Automotive category. We also only considered items that had some sort of electronic component. Since these items are newly released, many of them lacked substantial reviews and feedback; that’s normal at this stage. Reviews were helpful, but they were not a hard requirement. This round-up is simply a list of observations we’re keeping an eye on, not necessarily a list of recommendations. Use your best judgment when considering these products for your own ride setup.

Also worth noting: Pricing and availability are accurate at the time of this writing. These factors are subject to change at any time.

The “reverse Robin Hood” hypothesis is back, wearing a fresh econometric hat and carrying a very large number. The claim is familiar: credit card rewards programs let affluent cardholders pick the pockets of poorer consumers who pay with cash or debit. The new estimate is punchier. In a recent working paper, a group of academics argued that U.S. consumers who pay with cash and debit cards transfer roughly $30 billion annually to credit card users. Of that total, the authors estimate that $9.2 billion flows from households earning less than $150,000 per year to households earning more than that threshold.

Unsurprisingly, proponents of the Credit Card Competition Act, the Illinois Interchange Fee Prohibition Act, and a growing slate of state-level proposals have seized on the paper as fresh evidence that credit card rewards programs redistribute wealth upward. But the claim rests on some heroic assumptions about where people shop, what they buy, how merchants set prices, and whether cash is actually cheaper than cards. This post takes a more skeptical view.

The Reverse Robin Hood Story Hits a Speed Bump

The paper’s authors—Mark Egan, Gregor Matvos, Amit Seru, Lulu Wang, and Vincent Yao—deserve credit for building ambitious models and applying sophisticated econometric techniques to a pair of unusually rich datasets. In doing so, they avoid some of the more obvious methodological flaws that plagued the twoFederal Reserve Bank of Boston studies and theFederal Reserve Bank of Philadelphia study we criticized previously.

Those earlier papers advanced the familiar “reverse Robin Hood” claim: poorer consumers subsidize wealthier consumers through credit card rewards programs. As Egan et al. correctly observe, however, “[r]edistribution in the payment system requires consumers who use different payment methods to shop at the same stores.”

That is a surprisingly important point. Because the earlier studies lacked transaction-level data, they could not establish that cash-paying consumers and credit-card users were actually shopping at the same merchants. Having failed to clear that basic evidentiary hurdle, they could not demonstrate the redistribution they purported to measure.

Egan et al. at least partially solve that problem by combining firm-level card-settlement data from Fiserv—a merchant acquirer that processes card transactions—with establishment-level data from Clover, Fiserv’s point-of-sale platform. The Clover data includes card, cash, and check transactions for roughly 800,000 merchants. Using that data, the authors show that, by transaction value, credit-card users generally do not shop at the same stores as cash users.

Specifically, the authors note that, in the Clover dataset covering 2019 to 2022:

On average, cash accounts for around 11% of transaction dollars (dollar-weighted across merchants; Figure 2b). However, this masks substantial heterogeneity. For approximately two thirds of merchant-year observations, cash accounts for less than 2% of transactions. In contrast, for the one-third of merchants for which cash represents at least 2% of sales, it accounts for an average of 30% of their transactions—and for merchants in the 90th percentile, over 80%, highlighting the concentration of cash usage among a subset of merchants.

The implication is straightforward:

For the two thirds of firms where cash use is almost nonexistent, there is little scope for redistribution between cash and card users. Similarly, at firms where cash is the predominant payment method, redistribution is limited. Redistribution inherently requires a mixed payment environment, so dispersion in payment composition directly constrains the scope for cross-subsidization.

In other words, the “reverse Robin Hood” narrative about massive transfers from poorer cash users to wealthier credit-card users appears, at least initially, to stumble at the first hurdle.

The picture becomes more complicated, however—both for cash transactions, to which we will return later, and for the 89% of sales conducted through debit and credit cards. On that front, Egan et al. observe:

The distribution of credit card sales is bimodal, with peaks at approximately 25% and 70%. This bimodality suggests that although credit cards account for 53% of card transactions on average, merchants tend to fall into two distinct groups: those where credit accounts for around 25% of card transactions and those where it accounts for about 75%. This pattern has implications for cross-subsidization. Debit cards carry lower interchange fees and rewards relative to credit cards. Just as cash transactions can subsidize credit card rewards, debit card transactions also potentially play a subsidizing role. The bimodal nature of the distribution suggests that variation in card payment mix is significant at the merchant level—again limiting the potential for cross-subsidization, as many merchants are dominated by a single payment type.

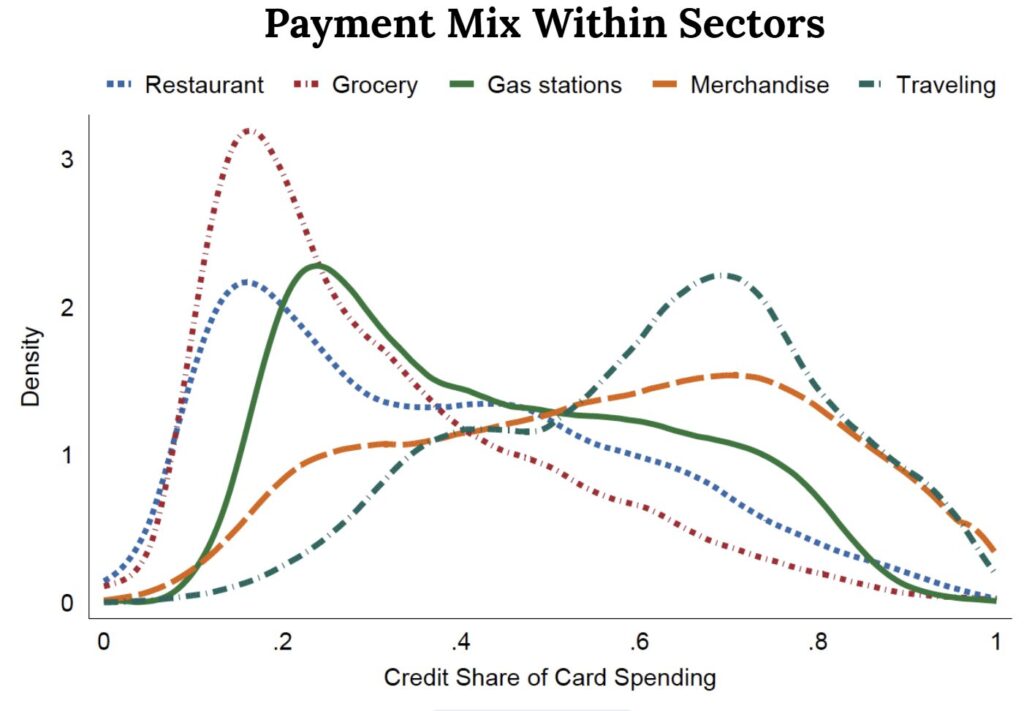

That finding suggests there may be some opportunity for cross-subsidization from debit-card users to credit-card users, particularly in sectors where debit and cash usage remain relatively high, such as grocery stores, gas stations, and restaurants.

Even there, though, the data point toward substantial sorting among customers. The figure below shows large peaks around 20% credit-card usage, followed by a long taper. Put differently, a relatively small subset of merchants accounts for a disproportionately large share of cash and debit transactions. As the authors explain: “This dispersion is important, as it implies that even within a given sector, consumers with different payment preferences tend to shop at different merchants, reinforcing the role of sorting in shaping redistribution.”

That further narrows the scope for meaningful within-store cross-subsidization. The aggregate figures reported by Egan et al. make the redistribution story appear more sweeping than the underlying merchant-level patterns likely support.

There is another complication the paper is unable to address: variation in what consumers purchase within the same store. Cross-subsidization is more likely if consumers using different payment methods purchase goods with similar margins and pricing structures.

The available evidence suggests that higher-income and more educated consumers systematically buy different products than lower-income consumers, particularly in grocery stores. Studies consistently find that wealthier consumers tend to purchase foods marketed as healthier or more premium, for example.

Grocery stores often earn higher gross margins on premium packaged foods,private-label “wellness” products, and other differentiated items than they do on commodity staples or national-brand basics. To the extent those higher-margin products are disproportionately purchased by credit-card users, the economics may run in precisely the opposite direction from the “reverse Robin Hood” story. Credit-card users could, in effect, be subsidizing lower-margin shoppers, including debit-card users.

More fundamentally, this illustrates a broader flaw in the “reverse Robin Hood” hypothesis. The theory isolates one component of merchant costs—interchange fees—while ignoring the larger pricing ecosystem in which merchants operate. What holds for grocery stores likely applies across many retail sectors. If wealthier consumers disproportionately buy premium goods and services, merchants can recover higher interchange costs through higher margins on those purchases, eliminating any meaningful cross-subsidy.

Indeed, many businesses operate on precisely that kind of variegated-margin model. Mainstream consumers provide scale and volume, while a smaller number of premium customers generate most of the profits. Airlines are the classic example: premium cabins effectively subsidize economy seating. Grocery stores and other retailers often operate in much the same way.

The Load-Bearing Assumption

This cuts directly to the question of pass-through. Egan et al. assume that merchants pass 100% of interchange costs through to consumers in the form of higher prices, although they include a sensitivity analysis that lowers the figure to 70%. Previous studies, by contrast—including those Ben Sperry and I reviewed here—generally find pass-through rates closer to 30%.

That difference is of crucial significance because the assumed pass-through rate underpins Egan et al.’s result; it is the load-bearing assumption. The authors are explicit: “in our baseline implementation of the sufficient statistic approach, we assume full pass-through of interchange fees to prices.” Without that assumption, the headline $30 billion redistribution estimate cannot be generated.

Their own robustness exercise underscores the point. When pass-through falls from 100% to a still-generous 70%, the estimated transfer to credit-card users shrinks by roughly one-third, to about $20 billion. The authors do not explore lower pass-through rates. Instead, they argue that the evidence supports something close to full pass-through. As discussed below, that claim is highly contestable.

The most sophisticated attempt to measure interchange pass-through directly remains Vladimir Mukharlyamov and Natasha Sarin’s study of the Durbin Amendment, which imposed price controls on debit-card interchange fees for banks with more than $10 billion in assets—so-called “covered banks.” The Durbin Amendment capped debit interchange at 0.05% plus fixed fees of $0.21 and $0.01 for fraud prevention.

Mukharlyamov and Sarin examined gasoline prices in areas with relatively high concentrations of covered banks and compared them to areas with fewer covered banks between 2009 and 2013—that is, two years before and two years after the Durbin caps took effect. They found evidence consistent with pass-through of roughly 28%, but the results were not statistically significant because gas prices were highly volatile during the period studied.

Egan et al. pursue a less direct strategy. Rather than examining prices themselves, they analyze spending patterns at restaurants. Specifically, they compare average spending per customer in ZIP codes with differing concentrations of covered-bank customers. In other words, they infer price effects indirectly through changes in demand.

One wrinkle is that the Durbin Amendment affected restaurant interchange fees in a non-linear fashion. Restaurants with small average ticket sizes sometimes saw interchange fees increase, because covered banks could apply the maximum fixed fee to all transactions. By contrast, restaurants with larger ticket sizes generally saw interchange fees fall because the capped percentage fee became a smaller share of the overall transaction.

Accounting for those effects, Egan et al. estimate that a one-percentage-point increase in interchange fees reduced restaurant sales by roughly 6.9%, which they interpret as implying approximately a 1.15% increase in average ticket size.

There is a problem, though: the paper’s pass-through framework operates at far too high a level of aggregation to capture how many merchants actually price goods and services.

Retailers and restaurants rarely apply a uniform markup across all products. Staples, entry-level products, and “traffic-driving” items are often sold at razor-thin margins—or even at a loss—to attract customers into the store. Premium goods, add-ons, discretionary purchases, and branded products typically carry much higher margins.

As a result, even if overall ticket sizes reflect some response to payment-acceptance costs, the incidence of those costs may differ dramatically depending on what consumers actually buy. If lower-income consumers disproportionately purchase staples, while higher-income credit-card users disproportionately buy premium products, desserts, alcohol, branded goods, or other high-margin items, then the effective incidence of interchange costs may be far less regressive than Egan et al. assume.

As already noted, the effect could even run in the opposite direction. Premium-product purchasers might bear more of the relevant costs, producing a “Robin Hood” effect rather than a “reverse Robin Hood” effect. This is a form of within-merchant sorting that the paper’s merchant-level framework cannot adequately capture.

The problem becomes especially acute in the paper’s restaurant analysis. Egan et al. do not observe menu prices or item-level purchases. Instead, they use average transaction size as a proxy for price.

But average ticket size can change for many reasons unrelated to price pass-through. Party size can change. Consumers may order more alcohol or desserts. More customers may dine in rather than order takeout. Tips may rise. The customer mix may shift. Payment-method composition may change. Most importantly for present purposes, credit-card users may simply purchase different products than debit-card users.

A rise or fall in average ticket size therefore cannot establish, by itself, that merchants adjusted menu prices one-for-one with interchange costs. It may instead reflect changes in purchasing composition or customer behavior. That is a significant limitation because the restaurant analysis serves as the paper’s principal evidence for broader claims about systemwide pass-through.

The paper also gives insufficient weight to the benefits merchants receive from accepting credit cards. Egan et al. largely treat interchange as a pure cost imposed on merchants and passed through to consumers. But credit cards also create substantial merchant-side benefits.

Most importantly, credit cards relax liquidity constraints. A cash user can spend only the money in her wallet. A debit-card user can spend only the funds available in her bank account. A credit-card user, by contrast, can spend against an available credit line. That can increase ticket size, facilitate larger purchases, and support higher-margin sales.

Interchange revenue also helps fund the bundle of features that makes credit cards attractive to consumers: fraud protection, zero-liability policies, chargeback systems, interest-free grace periods, rewards programs, purchase protection, travel insurance, and rental-car coverage.

Those features are not merely transfers to cardholders, as Egan et al. often imply. They also generate benefits for merchants who accept credit cards. The features encourage consumers to use credit cards, which may increase merchant profits. Analyses of payment systems have long recognized merchant benefits such as ticket lift, faster checkout, lower cash-handling costs, and reduced theft or skimming risk.

A real-world example illustrates the point. In 2018, Atlanta’s Mercedes-Benz Stadium became the first major U.S. sports venue to operate entirely cash-free. The following year, per-capita food and beverage sales rose 16%, wait times fell by 20 to 30 seconds, and operating costs declined by more than $350,000.

Similar patterns appear in grocery stores, quick-service restaurants, transit systems, and sports venues more broadly. Remove cash from the equation, and merchants often see higher revenue per customer. Yet Egan et al. treat interchange solely as a cost. They never seriously consider the possibility that merchants receive offsetting revenue benefits.

These considerations are especially important in the context of the Durbin Amendment, which capped debit-card interchange fees for covered banks, but left credit-card interchange untouched. Covered banks therefore lost much of their ability to fund debit-card rewards programs, free checking, and other debit-linked benefits.

Many banks responded exactly as one would expect: they eliminated debit-card rewards while preserving credit-card rewards. Consumers consequently had stronger incentives to shift spending from regulated debit cards to credit cards.

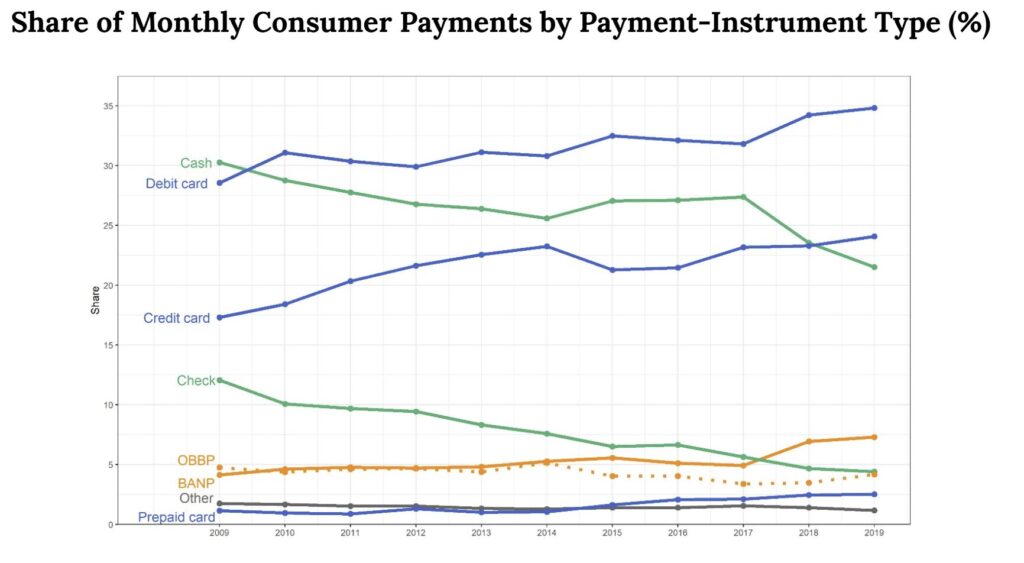

The available evidence suggests that is precisely what occurred. Federal Reserve survey data show that debit-card use declined and credit-card use rose significantly between 2010 and 2012, immediately following Durbin’s enactment, as shown in the figure below.

To the extent customers of covered banks shifted disproportionately from debit to credit, restaurants in ZIP codes with greater exposure to covered-bank customers would have experienced more than merely lower regulated-debit costs. They also may have experienced increases in credit-card usage, resulting in larger ticket sizes and other changes in purchasing behavior, including shifts toward higher-margin products.

If increased credit-card use generated ticket lift or encouraged purchases of premium goods, then some—or potentially much—of the observed revenue increase could reflect payment-method substitution rather than pass-through of lower debit interchange costs.

The upshot is that the restaurant evidence does not cleanly isolate pass-through. Instead, it may conflate several different mechanisms: the observed changes in debit acceptance costs plus unobserved shifts in payment-method use (including migration away from cash, which is unobservable because Egan et al do not have Clover data for the relevant period), ticket lift due to higher levels of credit card use in locations with greater proportions of covered banks, product-level pricing differences, and customer-composition effects.

Egan et al. assume fixed consumer payment preferences and model interchange primarily as a merchant cost passed through in a uniform way to retail prices. But if payment methods influence what consumers buy, how much they spend, and which products carry the highest margins, then the incidence of interchange becomes substantially more complicated than the paper allows.

At a minimum, average restaurant ticket sizes should not be treated as dispositive evidence of systemwide one-for-one pass-through. A convincing analysis would require item-level prices or baskets, total sales including cash transactions, and direct evidence regarding debit-to-credit substitution among customers of covered banks.

Cash Isn’t Free

Finally, let’s return to the question of cash.

Egan et al. explain that their analysis attempts to calculate transfers among different categories of payment users—and, by extension, among income groups—by comparing the current payment system to a hypothetical world with “zero interchange.” The paper correctly notes that merchants pay acquirers a merchant discount rate (MDR), which covers not only interchange fees remitted to issuing banks, but also other payment-processing costs.

The implicit assumption is that, absent interchange fees, merchants would simply pay this lower baseline MDR on all transactions. For the roughly two-thirds of merchants whose transactions are almost entirely electronic, that assumption is reasonably plausible.

For the remaining third of merchants—those where cash accounts for more than 2% of payments—it is anything but plausible. In many cases, it is simply wrong.

The reason is straightforward: cash may avoid interchange fees, but handling cash is expensive.

The most comprehensive recent study of cash-handling costs was conducted by IHL in 2018. The study identified nine major categories of cash-related expense:

Start/rebuild drawer costs associated with opening and resetting cash drawers;

Closing-drawer reconciliation and counting;

Cash pickups during shifts;

Change-order management;

Audits and discrepancy resolution;

Preparing and coordinating deposits;

Cash-in-transit and bank-deposit costs;

Bank fees and related charges; and

Cash shrink, including theft, fraud, and unexplained losses.

Once those costs are fully accounted for, IHL estimated that cash handling costs merchants between 4% and 15% of transaction value.

By comparison, the only directly comparable costs for electronic payments are cashier time during payment acceptance and certain bank-service fees that supplement the merchant discount rate. In most cases, the all-in cost of cash transactions equals or exceeds the cost of debit or credit transactions.

Earlier work points in the same direction. Daniel D. Garcia-Swartz, Robert W. Hahn, and Anne Layne-Farrar found that, for typical grocery-store purchases, cash transactions cost more than either credit or debit transactions. Even for transactions as small as $12, cash cost roughly the same as credit and more than debit.

More recent research reaches similar conclusions. The Federal Reserve Bank of San Francisco’s 2019 paper “Cash Me If You Can” concluded that “cashless operations help businesses save on cash handling costs, reduce exposure to theft, and increase the speed of transactions.”

Our own review reached the same bottom line: once all parties to the transaction are considered, electronic payments are generally less costly than cash for most transactions—not the other way around.

That makes Egan et al.’s suggestion that cash users subsidize credit- and debit-card users difficult to sustain. If anything, the economics more likely run in the opposite direction.

The paper’s accounting problem extends beyond merchant costs. Egan et al. also omit—or treat merely as transfers—a long list of benefits funded through interchange revenue.

Those benefits include the fraud-liability protections established under Regulation Z, which caps consumer liability for unauthorized credit-card transactions at $50 and, in practice, usually at zero. They include chargeback and dispute-resolution systems that function as a form of purchase insurance unavailable to cash users or users of direct bank-transfer systems.

They also include the interest-free grace period attached to credit cards. Consumers who pay their balances in full each month effectively receive a short-term, unsecured, zero-interest loan. That is not a trivial convenience. For many lower-income households managing uneven cash flow, it is a genuinely valuable financial tool—and one available regardless of income, FICO score, or financial sophistication.

Credit cards also provide emergency access to liquidity. An available credit line can function as a substitute for precautionary savings, which matters most for households with limited liquid assets.

Then there is the infrastructure itself. Interchange revenue helps fund tokenization, EMV chip technology, contactless payments, 3D Secure authentication, real-time fraud detection, and the broader payment-network innovations consumers now take for granted.

For the very populations the “reverse Robin Hood” narrative purports to protect, these are not incidental benefits. They are first-order features of the system.

A redistribution analysis that ignores them is not merely incomplete. It is measuring the wrong thing altogether.

The Reverse Robin Hood Story Has It Backwards

Putting all this together, the “reverse Robin Hood” story largely falls apart. There may be some degree of cross-subsidization from debit-card users to credit-card users, driven in significant part by the distortions introduced by the Durbin Amendment. But the much larger effect likely runs in the opposite direction: from electronic-payment users to cash users.

Because cash transactions are disproportionately associated with lower-income consumers, that dynamic looks a lot more like Robin Hood than reverse Robin Hood. Wealthier consumers who use premium credit cards help fund a payments ecosystem that lowers costs and expands functionality for everyone else.

So how do Egan et al. arrive at such a different conclusion?

Part of the answer appears on the opening page of the paper itself. The authors argue that: “Existing debates often frame interchange as either a ‘tax’ on merchants or a mechanism to fund consumer rewards. Both views overlook that interchange fees primarily redistribute consumption across consumers …” (p.1).

But that framing omits a crucial fourth possibility—one the authors themselves acknowledge later in the paper:

Fee variation across sectors reflects Visa’s and Mastercard’s attempts to balance merchant acceptance versus issuer incentives, trading off participation on both sides of the platform.

That is not some secondary observation buried in the weeds. It is the core economic logic of payment-card networks.

Ever since William Baxter’s seminal 1983 work, economists have understood payment systems as classic two-sided markets. Jean-Charles Rochet and Jean Tirole later formalized the insight. Payment networks must attract both merchants and consumers simultaneously. Interchange fees function as the balancing mechanism that keeps both sides participating.

The goal is not redistribution for its own sake. The goal is maximizing the value of the platform across both sides of the market.

Merchants receive faster checkout, higher throughput, lower cash-handling costs, fraud protection, guaranteed payment, and larger ticket sizes. Consumers receive convenience, security, recordkeeping, zero-liability protection, access to credit, and—in the case of premium credit cards—rewards and ancillary benefits that make card use more attractive.

Interchange is the mechanism that funds that ecosystem. It supports issuer investment, fraud prevention, credit risk management, and the incentives that encourage consumers to adopt electronic payments in the first place.

That pricing structure has played a central role in the remarkable migration away from paper-based payments over the past two decades. Cash and checks have steadily given way to cards because electronic payments became faster, safer, more convenient, and often less costly for both sides of the transaction.

Federal Reserve data show the trend continuing. Cards accounted for roughly 66% of transactions in 2025, up from 45% in 2009. Cash usage, meanwhile, fell from roughly 30% to just 13%.

Premium credit cards have been an important driver of that transition. Higher-value cards use interchange revenue to fund rewards, insurance, fraud protections, and related benefits that induce consumers to participate more heavily in electronic-payment systems. Greater consumer demand, in turn, increases the value of card acceptance to merchants, encouraging adoption of innovations such as contactless payments and increasingly cashless retail environments.

That dynamic remains important because cash still retains advantages for some consumers and some transactions. As the Federal Reserve recently observed:

Despite a small decline from last year, the consistent use of cash year-over-year shows there are certain transactions where people want or need to use cash. This is likely due to several unique characteristics of cash payments that other payment options have yet to fully replicate, such as anonymity, widespread acceptance, instant settlement and reliability as a secondary payment instrument.

In other words, the migration away from cash is incomplete. Premium credit—and potentially more competitive debit products—still plays an important role in encouraging consumers to adopt electronic payments and helping merchants move away from expensive cash-handling systems.

Indeed, one implication of this analysis is that policymakers should seriously reconsider the Durbin Amendment itself, or at minimum relax the Federal Reserve’s interchange caps on covered banks. Doing so would allow debit cards to compete more effectively against both credit cards and cash.

That could benefit lower-income consumers directly through expanded checking-account access and richer debit-card rewards, both of which would promote financial inclusion and reduce reliance on cash. Merchants would benefit as well if more consumers shifted back toward debit, which generally carries lower acceptance costs than credit.

The irony, then, is that the policies sold as fixes for “reverse Robin Hood” redistribution may well undermine one of the most successful financial-inclusion and payments-modernization systems ever created. Sometimes the supposed subsidy story turns out to be the reverse.

To provide the best experiences, we use technologies like cookies to store and/or access device information. Consenting to these technologies will allow us to process data such as browsing behavior or unique IDs on this site. Not consenting or withdrawing consent, may adversely affect certain features and functions.

Functional

Always active

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.