As solid-state drives (SSDs) slowly replace traditional hard drives’ spinning platters, portable data storage has become far more reliable. I remember the days of lugging hard drives outdoors where they were prone to getting bashed around, exposed to dirt, water, and all sorts of grime. All it took was one unfortunate spill or knock to render your storage useless and throw a huge wrench into an otherwise smooth day.

What I would have given back then for storage that had no moving parts, wouldn’t break when knocked around, and could be housed in an enclosure that’s practically bombproof. Enter: the Terramaster D1, a portable SSD enclosure that delivers all this — and at a competitive price.

Terramaster is a well-established brand with a long-standing reputation in the data storage industry. I’ve trusted their NAS boxes for years, so when I got the chance to try their new portable enclosure, I didn’t hesitate. What I didn’t know at the time was just how tough this little enclosure would turn out to be.

This is a very well engineered enclosure with really good gaskets.

Adrian Kingsley-Hughes/ZDNET

The Terramaster D1 is small enough to fit in your pocket, measuring just 4.5 x 1.8 x 0.8 inches and weighing a little over five ounces (without a drive). Once you add an M.2 2280 NVMe SSD, you’re looking at just about half an ounce more. The enclosure supports drives up to 8TB and delivers read/write speeds of up to 10Gbps, or roughly 1,010MB/s (testing done using a Samsung 990 Pro SSD).

Of course, your final speeds will depend on the quality of the M.2 NVMe SSD you install and your host system. A $60 SSD will perform differently than a $600 one.

It’s all about how much you’re willing to spend. I should note that the D1 only supports 2280 NVMe SSDs. That means 2230, 2242, 2260 drives, or SATA SSDs won’t fit.

Serious durability

All this merely scratched the drive up.

Adrian Kingsley-Hughes/ZDNET

If the D1 were just a sleek, fast enclosure, I’d already consider it a great product. But what sets it apart is its tough-as-nails build quality.

The enclosure is crafted from aerospace-grade aluminum alloy, which is lightweight, corrosion-resistant, and incredibly durable. It can withstand crushing pressures up to 1.2 tons, making it ideal for rugged environments. The aluminum construction also doubles as a heat sink, dissipating the heat generated by high-performance SSDs.

The enclosure’s design maximizes surface area to further aid in heat dissipation, and Terramaster has even included a thermal pad inside for additional efficiency.

Just one screw holds the enclosure together (screwdriver supplied).

Adrian Kingsley-Hughes/ZDNET

Beyond the physical toughness, the D1 is also IP67-rated for dust and water resistance. This means it’s submersible in up to one meter of water for 30 minutes — as long as the enclosure is fully sealed, with the covers aligned, gasket intact, and screws tightened. Just be careful not to lose the tiny silicone port cover.

I fear this tiny port cover will get soon get lost.

Adrian Kingsley-Hughes/ZDNET

I gave the drive a good hammering, throwing it about, standing on it, and driving a digger over it (not as impressive as it sounds since it spreads the wight across the whole surface area of the tracks).

This enclosure can take over a ton of crushing force.

Adrian Kingsley-Hughes/ZDNET

This is a very robust enclosure.

Adrian Kingsley-Hughes/ZDNET

Compatibility and backup features

The Terramaster D1 is compatible with Windows, MacOS, Linux, iOS, and Android, making it a versatile tool for users across platforms. If you’re using an iOS or Android device, you can download the TDAS Mobile app (iOS/Android), which allows you to perform one-click automatic backups of your photo albums.

This is the enclosure after a lot of abuse. Only a few scratches.

Adrian Kingsley-Hughes/ZDNET

This feature is a lifesaver for anyone looking to free themselves from the ongoing costs of cloud storage while keeping their data safe and secure.

ZDNET’s buying advice

The Terramaster D1 is a standout SSD enclosure that combines impressive durability, speed, and portability. With its aerospace-grade aluminum construction, IP67 water and dust resistance, and blazing-fast data transfer speeds, it’s a no-brainer for anyone in need of reliable portable storage.

And the price is right: $39.99. Yes, that’s right. Forty bucks.

I’d recommend this to professionals working in the field, digital nomads, or anyone who values their data and is tired of fragile storage solutions. Additionally, anyone who wants to stop overpaying for cloud storage will find the D1 delivers everything you could want in a rugged enclosure — at a price that feels like a steal.

Here’s a number that should stop you mid-scroll: India’s gross NPA ratio hit a historic low of 2.15% as of September 2025 — the lowest level since 2010-11, confirmed by the RBI in its latest Trends and Progress of Banking in India report released December 2025.

Now here’s the number that puts it in context: the absolute gross NPA stock still stood at ₹4.32 lakh crore.

That gap — between a ratio that looks reassuring and an absolute number that demands serious infrastructure — is exactly where India’s debt collection industry lives in 2026. The headline is good. The operational challenge is not over. And the technology being deployed to close that gap is transforming the industry faster than most lenders have internalized.

Understanding India’s NPA story in 2026 requires holding two truths at once.

The first truth: asset quality has genuinely improved. Public sector banks saw their gross NPA ratio fall from 9.11% in March 2021 to 2.58% by March 2025. Net NPAs are at 0.5%. The slippage ratio — which measures fresh loans turning bad — declined for the fifth consecutive year to 1.4% at end-March 2025. By almost every ratio-based metric, this is the healthiest India’s banking sector has been in a generation.

The second truth: the composition of what’s left has changed dramatically. The easy-to-resolve large corporate NPAs have largely been worked through the IBC pipeline. By March 2025, more than 30,000 applications representing underlying defaults of ₹13.78 lakh crore had been settled at the pre-admission stage alone. What remains is a harder, more distributed problem — retail loans, MSME advances, microfinance accounts, scattered across geographies, ticket sizes, and legal jurisdictions. India’s loan book crossed ₹2.2 trillion in FY25, with personal loans alone doubling from 73 million to 146 million accounts in three years.

More loans at smaller ticket sizes, more borrowers who are first-time credit users, more accounts that fall into DPD buckets without the ability to recover through traditional legal channels. The ratio looks good. The recovery work is just beginning.

Technology Has Stopped Being Optional

If 2023 was when collections technology became mainstream, 2026 is when it became existential. The proof is in the adoption curves.

Mid-sized banks observed a 34–36% drop in credit disbursement and collection costs due to AI adoption. Institutions implementing AI-driven collections strategies report recovery rate improvements of 10–25% and significant reductions in operational costs. AI adoption in finance functions has climbed to 59% of firms globally — up from just 37% in 2023.

In India specifically, the pattern is clear: platforms that started with digital nudges and payment reminders have graduated into full-stack recovery infrastructure. Credgenics, which recently partnered with Aye Finance, now combines omnichannel communication with AI-powered borrower scoring, a litigation management system, and an ODR capability — covering the collections lifecycle from the first payment reminder to settlement. DPDZero has built intelligent early-stage workflow automation with strong pre-legal capabilities. Both represent real progress on the front end of the collections funnel.

Industry leaders entering 2026 are clear that AI will act as a major catalyst across servicing, collections, underwriting support, and operational efficiency — with customer-facing adoption following with the right regulatory safeguards in place.

But here is where the story gets more nuanced: most of the AI investment in Indian collections has been concentrated in the 0–90 DPD bucket. The pre-legal stage. The moment a borrower crosses into formal legal territory — a SARFAESI notice, a DRT filing, a Section 138 cheque bounce case — the sophistication level drops sharply. Legal recovery in 2026 is still largely manual at most lenders, tracked through spreadsheets, coordinated over WhatsApp, and measured through gut feel rather than data.

This is the infrastructure gap that defines the next wave of collections technology in India.

Where The Legal Stack Is Breaking

Legal recovery was never meant to be the last resort. Under SARFAESI, lenders have the right to take possession of secured assets without court intervention. Under the IBC, creditors have genuine leverage. Debt Recovery Tribunals were specifically designed to fast-track financial disputes.

The frameworks work. The execution doesn’t — not at scale.

Consider what a legal recovery workflow typically looks like at a mid-sized NBFC with 5,000 NPA accounts: notices are drafted in batches, manually checked, dispatched through India Post without systematic delivery tracking. Court hearing dates live in someone’s calendar. Advocate assignments are based on familiarity rather than performance data. If a case gets adjourned three consecutive times with no action, there’s often no automated alert. The account drifts.

Over 320 new debt recovery platforms launched between 2022 and 2024 offering integrated dashboards, cloud-based workflows, and multilingual customer engagement. Yet very few of these have solved the legal layer — jurisdiction-specific notice templates that pull directly from loan management data, court case tracking that flags at-risk hearings, advocate performance analytics that tell you which empanelled lawyer closes DRT cases fastest in a specific geography.

Platforms built specifically for the collections-to-legal junction are filling this gap. Legodesk’s infrastructure, for instance, is purpose-built around exactly this workflow: legal notice automation with India Post integration and tracked delivery, centralized court case management across DRT, NCLT, and civil courts, and advocate network analytics that surface performance data rather than just contact information. The goal is to make the legal recovery process as operationally tight as pre-legal collections has become — auditability built in, data flowing both ways, outcomes measured.

The Regulatory Ratchet Is Only Moving One Way

The regulatory environment in 2026 is not getting simpler. The Digital Personal Data Protection Act, now operationalized through sector-specific guidelines from RBI, SEBI, and IRDAI, has fundamentally changed how lenders must architect their data flows, consent management, and vendor relationships. Regulation is emerging as a structural force rather than a cyclical hurdle for Indian fintechs entering 2026.

In collections specifically, this translates to: contact hour restrictions that require systematic enforcement, documentation requirements that demand automated audit trails, and borrower communication protocols that need to be embedded in the platform rather than left to individual agent discretion.

The lenders best positioned for this environment are the ones who treated compliance infrastructure as a capability investment rather than a cost center. Automated legal notice dispatch — where every notice is templated, timestamped, and tracked — is not just operationally efficient. It is legally defensible in a way that manual processes are not. When the RBI or a DRT asks for evidence of process, a documented digital trail answers that question in minutes. A WhatsApp archive does not.

The Emerging Recovery Ecosystem

One of the more interesting structural shifts in India’s collections space over the last 18 months is the move away from “one platform for everything” thinking toward ecosystem thinking.

Different parts of the recovery journey call for genuinely different capabilities. Pre-litigation resolution through platforms like Presolve360 is creating real value for smaller-ticket disputes — ODR and mediation reduce the burden on formal legal channels for accounts where SARFAESI or DRT proceedings would cost more than the debt itself. Early-stage collections automation from platforms like DPDZero works best when it’s connected to legal escalation triggers rather than operating as an isolated system. Legal management infrastructure like Provakil serves the enterprise legal function well, even where it isn’t collections-specific.

The lenders achieving the best recovery outcomes are not choosing between these. They are building recovery stacks — thinking clearly about what capability handles which stage of the journey, where data needs to flow between systems, and what the handoff protocol looks like when a borrower moves from pre-legal to legal territory.

This ecosystem mindset is relatively new in India. It is where the industry is headed in 2026, and the lenders who get there first are building a durable operational advantage.

What The Number Actually Tells You

Back to that opening statistic. A 2.15% NPA ratio is a genuine achievement — the result of eight years of sustained effort across regulatory reform, IBC implementation, recapitalization, and increasingly sophisticated recovery operations.

But ₹4.32 lakh crore in absolute gross NPAs, sitting in a loan book that is growing at double digits annually, with a retail and MSME composition that requires more distributed, technology-intensive recovery operations than anything India’s collections industry has managed before — that is not a problem that a good ratio solves.

It is a problem that infrastructure solves. And in 2026, the infrastructure is finally being built.

Legodesk provides legal recovery infrastructure for banks, NBFCs, and fintechs — connecting collections workflows with legal notice automation, court case management, and advocate network analytics. Contact us

FAQs

What is India’s current NPA ratio in 2026?

India’s gross NPA ratio reached a historic low of 2.15% as of September 2025, according to RBI data confirmed in February 2026. In absolute terms, gross NPAs stood at approximately ₹4.32 lakh crore as of the same period.

How is AI being used in debt collection in India?

AI is being deployed across predictive default scoring, omnichannel borrower communication, automated legal notice dispatch, and court case management. Mid-sized banks have reported a 34–36% reduction in collection costs after AI adoption, with recovery rate improvements of 10–25%.

What laws govern debt recovery in India?

How is AI being used in debt collection in India? A: AI is being deployed across predictive default scoring, omnichannel borrower communication, automated legal notice dispatch, and court case management. Mid-sized banks have rep

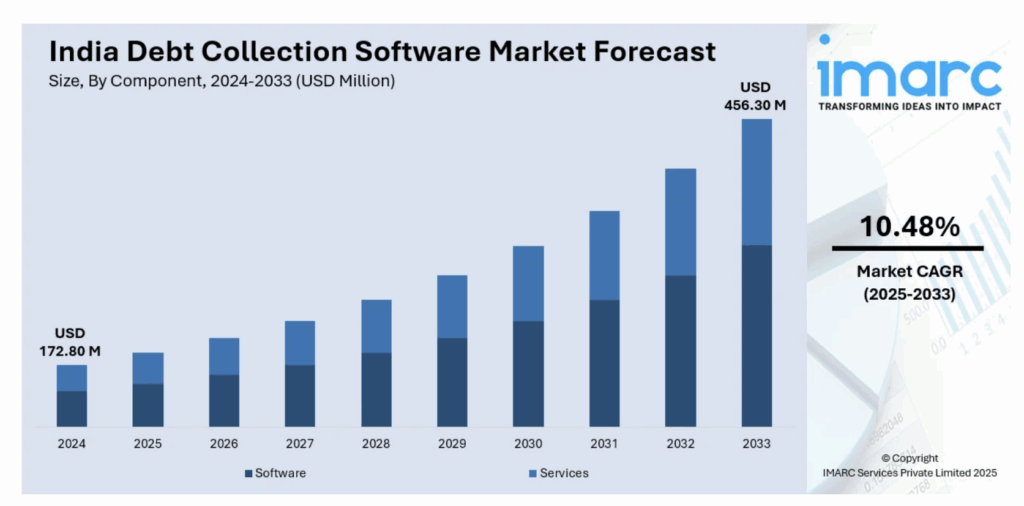

What is the size of the debt collection software market in India?

India’s debt collection software market reached approximately $172.8 million in 2024 and is projected to grow to $456 million by 2033 at a CAGR of 10.48%, per IMARC Group.

To provide the best experiences, we use technologies like cookies to store and/or access device information. Consenting to these technologies will allow us to process data such as browsing behavior or unique IDs on this site. Not consenting or withdrawing consent, may adversely affect certain features and functions.

Functional

Always active

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.