Trump says Powell has been too tight. The data says the opposite. Powell has run the easiest monetary policy in modern Fed history, and the credibility cost is what makes the institution so vulnerable today

Later today the Federal Open Market Committee will almost certainly leave its target range for the federal funds rate unchanged at 3.50 to 3.75%, and markets are pricing a 100% probability of the hold. The only suspense in the room is whether Stephen Miran dissents again, as he did at the March meeting, in favour of a quarter-point cut.

That is the part everyone agrees on. The interesting question, in my view, is everything else – and the ritual focus on the rate decision actually obscures what is happening in the institution today.

This is, in all likelihood, Jerome Powell’s final meeting as Federal Reserve chair, with his term ending on May 15. Kevin Warsh has been nominated by the President to replace him, and the Senate Banking Committee is voting on the nomination this morning (US time), four hours before the FOMC’s own decision.

The political timing is, of course, not an accident. Last week the U.S. attorney for the District of Columbia, Jeanine Pirro, transferred her investigation of the renovations at the Fed’s headquarters to the Fed’s own office of inspector general – a procedural move that cleared the obstacle Senator Thom Tillis had placed in front of the Warsh nomination.

So here is what Wednesday actually is. It is not a rate decision. It is the end of an era at the Federal Reserve, and the beginning of a regime under conditions that have not existed in the United States since Arthur Burns sat in the chair.

What the dual-mandate framing misses

The Fed’s dual mandate looks roughly balanced if you are willing to squint at it. Core PCE inflation is running around 3%. The labour market is soft but not collapsing – weak hiring, unemployment at 4.3%, and payroll growth that has slowed without breaking. Brent oil is around $110 a barrel. The energy shock is not yet fully fed through to headline inflation.

That is a reasonable summary of the technical position. And it is also, in my view, almost beside the point.

The Fed has been above its 2% inflation target for five years. Five years. There is no recent precedent for a major central bank running this far above target for this long without either delivering the disinflation or formally rebasing the target. The institution has done neither. It has waited. The technical case for waiting is fine. The institutional consequence of having waited for five years is something else entirely.

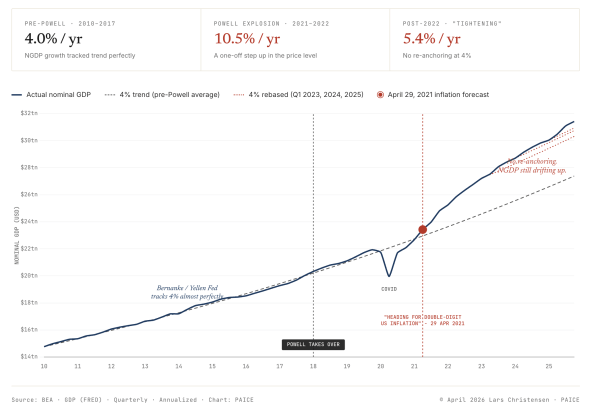

A picture of the failure

Trump has spent the past year arguing that Powell has run policy too tight. The data tells the opposite story.

The chart below shows nominal GDP, in level terms, from 2010 through the end of 2025. The dashed grey line is a 4% growth trend anchored at the start of the period.

I have argued for years that the post-2008 Federal Reserve under Ben Bernanke and Janet Yellen ran a de facto 4% NGDP target, and that this target was broadly consistent with their stated 2% PCE inflation objective, given underlying productivity and labour-force growth.

Look at what the picture shows.

From 2010 through the end of 2017, US nominal GDP grew at almost exactly 4% per year. The actual line and the trend line are essentially indistinguishable. This is what a predictable monetary regime looks like – the price level and real output combined growing at a steady, predictable rate that markets can plan around.

Powell took over in February 2018.

NGDP continued at roughly 4% growth through 2019. The Covid shock in Q2 2020 produced a sharp negative deviation, and the Fed’s response in March 2020 was, in my view, exactly right. By the end of 2020, NGDP was already approaching the trend line again.

Then came 2021.

The April 2021 forecast

On this day five years ago, April 29, 2021, I published a blog post on this blog titled “Heading for double-digit US inflation.”

I want to quote what I actually wrote, because the framing matters.

I argued at the time that the explosion in US broad money supply, combined with the largest fiscal expansion since the Second World War, would produce a sharp one-off jump in the US price level – not necessarily a permanently higher inflation rate, but a level shift that would be very fast and very large.

I wrote that the fixed-income market was mispricing the inflation risk. I noted that the Fed seemed to be deliberately behind the curve. And I wrote that what would happen after the price level jump would depend entirely on the Fed’s response.

Either the Fed would move aggressively to anchor expectations and contain the shock as a one-off, or it would allow a serious erosion of credibility and longer-term inflation expectations would jump as well.

That was the forecast. The red dot on the chart marks where it was made.

The forecast was correct on the inflation outcome. Headline CPI inflation peaked at 9.1% in June 2022 – the highest rate of inflation in four decades. The forecast was correct on the timing – the price level moved fast and sharply through late 2021 and 2022.

The point is not that I got the forecast right. The point is that the forecast was available to anyone willing to read the data.

The P-star model I used was developed by Hallman, Porter and Small at the Federal Reserve in 1989. The broad money numbers were public.

The fiscal arithmetic was public. The relationship between monetary expansion and subsequent inflation, with the lags Milton Friedman had identified decades earlier, was textbook material. The Federal Reserve had access to all of this information, employed dozens of monetary economists with sophisticated models, and was looking directly at the same data I was looking at.

And the Federal Reserve, under Powell, chose to do nothing.

Worse than nothing. The Fed had, in 2020, adopted a new framework called Flexible Average Inflation Targeting – FAIT – which committed the FOMC to running inflation moderately above 2% for some period after running it below 2%. The framework was defensible in theory. The application in practice was a catastrophe.

Through 2021 and into early 2022, the Fed held the funds rate at zero and continued QE asset purchases at $120 billion per month even as nominal GDP growth ran at 11% in 2021 and nearly 10% in 2022. Pre-Powell average growth was 4%. Powell’s Fed ran NGDP growth at more than two-and-a-half times the established regime rate.

That is not flexible average inflation targeting. That is, as I have written elsewhere, the monetary policy equivalent of price fixing – holding the policy rate so far below its market-clearing level that the resulting inflation was not an accident but a mechanical consequence.

Powell’s Fed told the public, repeatedly, that the inflation that was already arriving was transitory. The word was, by late 2021, no longer defensible on any reasonable reading of the monetary indicators. It was deployed anyway, and the Fed maintained the framing through most of 2021 and into early 2022, well after the empirical case for it had collapsed.

This was not a close call. This was not a difficult judgement. This was the textbook monetary failure – too much money chasing too few goods, with the central bank insisting that money does not matter and that the inflation will go away on its own.

The reversal that did not anchor anything

Powell then spent 2022 and 2023 trying to undo the damage. From a target range of 0-0.25% in March 2022, the Fed reached 5.25-5.50% by July 2023. Inflation came down, and the labour market did not collapse. That was, by historical standards, a successful disinflation – one of the few things from the Powell era that I will give him unambiguous credit for.

But here is where the chart tells a story that the press releases do not.

Look at the three red dotted lines on the chart. Each one is a 4% trend rebased at a different starting point – Q1 2023, Q1 2024, and Q1 2025. They show what NGDP would have done if Powell’s Fed, having allowed the price-level jump, had at least re-anchored the growth rate at 4% from each of those points forward.

The actual path lies above all three.

I am not, to be clear, arguing that Powell should have tried to bring NGDP back to the original pre-2020 trend. That would require at least a Paul Volcker-scale disinflation, and the current fiscal arithmetic – debt above 100% of GDP, interest payments above $1 trillion – makes that mathematically impossible without causing a US sovereign default (more on that below). The price-level jump is permanent. We have to live with it.

But the growth rate is a separate question. After the price-level jump, the Fed could have re-anchored at 4%. It chose not to. From Q1 2023 to today, NGDP growth has averaged 5.4% per year – 1.4 percentage points above the established regime rate. From Q1 2025 alone, the rate is 6.2%. The growth rate is, if anything, drifting higher rather than settling.

So the Fed in 2025 and 2026 is not running a tight policy that has finally restored discipline. It is running a policy that continues to accommodate above the long-run trend. Powell tightened relative to the catastrophe of 2021-22, yes.

But he has not returned the regime to anything resembling the Bernanke-Yellen anchor. The “tightening” is in scare quotes for a reason. It is tightening relative to the Fed’s own previous error, not tightening relative to a credible monetary framework.

The Burns parallel

The historical episode that maps most directly onto the current situation is the early 1970s. President Nixon, facing reelection in 1972, applied direct and well-documented pressure on Federal Reserve Chair Arthur Burns to ease monetary policy. The Nixon tapes contain explicit instructions – not requests, instructions – that Burns increase the money supply ahead of the election.

Burns complied. He explained, meeting by meeting, why the next move would have to wait, and each individual decision sounded reasonable in isolation. The cumulative result was a decade of inflation, requiring a Volcker disinflation that took unemployment to nearly 11% to break.

The Burns analogy applies to Powell only partially. He raised rates aggressively in 2022 and 2023, the disinflation was real, and he resisted Trump’s public pressure throughout the second Trump term. He has not been Burns on the political-pressure dimension.

But on the analytical dimension – the willingness to ignore the inflation indicators when the prevailing framework said not to act – the parallel is uncomfortably close.

Burns ignored the monetary aggregates because his framework said they did not matter. Powell ignored them in 2021 because FAIT said the inflation was wanted. The institutional failure has the same shape, even if the specific theoretical justifications differ.

The cost of the failure is what we are living through

Here is the structural problem the dual-mandate framing does not capture, and which I think is the single most important thing about the current moment.

Trump has spent the past year publicly arguing that Powell has run policy too tight, that interest rates should be lower, and that the Fed has been hostile to the administration. The chart above shows that the empirical case for this is essentially nil. Powell has run the easiest monetary policy in modern Fed history. NGDP growth has been substantially above the regime rate since 2021. The federal funds rate is below where most reasonable models would put neutral, given the inflation conditions of the past five years.

So why does the political attack land?

It lands because the Fed has, over the same period, demonstrated in real time that it cannot be trusted to act on the inflation indicators when its preferred theoretical framework tells it not to. The credibility deficit Warsh inherits is not just a number. It is the gift that the Powell Fed has handed to anyone, including Donald Trump, who wants to argue that the institution does not deserve the deference that has historically been extended to it.

A Fed that had not produced 9% inflation in 2022 – because it had read the broad money data correctly in 2021 and acted on it – would now be defending its independence from a position of overwhelming strength. Trump’s attacks would land in empty air. Markets would dismiss them. Congressional Republicans would be reluctant to follow.

Instead, the Powell Fed defended independence from a position of partial credibility, after producing a major inflation that the public and the political branch had to absorb. The independence defence has held so far. But the defence is much weaker than it would have been, and the institution is much more politically vulnerable than it would have been, because of the 2021 failure.

This is the link between the easy monetary policy of 2021 and the political crisis of 2025-26 that almost no commentator is drawing. They are not separate stories. They are the same story.

The fiscal-dominance story

Federal debt held by the public now exceeds 100% of GDP. Net interest payments on the federal debt have surged from about $350 billion in 2020 to over $1 trillion in 2025.

Every 100 basis points of higher policy rates adds roughly 1% of GDP to the federal interest bill over time. The federal government has a powerful, mechanical reason to want lower rates – independent of whether lower rates are appropriate for the macroeconomy.

Trump has been remarkably explicit about this. He has stated publicly, more than once, that lower rates would help the federal budget. He simply wants lower rates, and I think he wants them for fiscal reasons, not for macroeconomic ones.

This is the condition economists call fiscal dominance – a regime in which the fiscal authority’s needs constrain the monetary authority’s ability to conduct independent monetary policy.

It is, in fact, the structural condition behind essentially every major historical inflation episode I can think of, from the German hyperinflation of 1923 through the Latin American inflations of the 1970s, the post-Soviet inflation in Russia, the chronic Argentine inflation, and the Turkish episode under Erdoğan. The 1970s American and European inflations were milder versions of the same dynamic.

What changes with Warsh

Some have argued that Kevin Warsh will be a hawk because he dislikes QE, and that reading is, in my view, partly right and substantially wrong at the same time.

The right part first. Warsh was a Fed governor from 2006 to 2011, and he has, as a private citizen, been a critic of the Fed’s enlarged balance sheet and of what he has called mission creep into financial-stability and macroprudential territory. Those are positions I have considerable sympathy for.

What economists call The Tinbergen rule says that each policy target requires its own policy tool, and a central bank that pursues price stability, full employment, and financial stability all at once – while adding new macroprudential objectives on top – is going to do at least one of them badly.

Goodhart’s Law adds the further point that when a measure becomes a target, it ceases to be a good measure. The macroprudential indicators the Fed has been adding to its toolkit are precisely the kind of measures Goodhart’s Law was written about.

So a Warsh chairman who shrinks the institutional ambition of the Fed and pushes back on macroprudential creep is, in my view, doing useful work, and I would actively welcome that part of the transition.

The wrong part, and the more important part, is what Warsh proposes to replace it with. And here, in my view, the answer is that he does not propose anything specific.

Warsh’s diagnosis of where the Fed has gone wrong over the past 15 years is the easiest part of the analysis. What is missing is the framework that would replace the discretion he wants to remove.

He has not said what monetary policy rule he wants the Fed to follow. He has not said how he would handle the next zero-lower-bound episode. He has not said whether he prefers inflation targeting, NGDP targeting, price-level targeting, or something else. He has not said how he would respond if the federal government pushed the debt above 130% of GDP and demanded accommodation.

Warsh’s IMF speech from April 2025 was, in many ways, a job application written for Trump’s ear – a list of grievances about institutional drift, paired with suggestive language about Federal Reserve independence that pointed in the direction of less independence rather than more.

There is also, frankly, the family dimension. Warsh is married to Jane Lauder, daughter of Ronald Lauder, who is a long-standing personal friend of Donald Trump.

Under normal circumstances I would consider this irrelevant. But these are not normal circumstances. The President has spent the past year publicly demanding lower rates.

The investigation into Powell was, by most credible accounts, a political pressure tactic. So when the President’s preferred candidate to replace the chair turns out to have a family connection to the President’s inner circle, that fact deserves to be on the analytical record.

The Friedmanite reading

I take a fairly simple lesson from all of this, and it is the point on which I want to land.

Milton Friedman wrote, in his Nobel lecture and many times before and after, that monetary policy works with long and variable lags and cannot reliably fine-tune the economy. Scott Sumner has updated this with the observation that monetary policy works with long and variable leads, because the transmission runs through expectations rather than through mechanical adjustments to short rates.

Both formulations point to the same institutional conclusion: what matters is the regime, not the meeting-to-meeting decisions. A Fed that has spent five years being technically careful about each individual meeting has lost sight of the regime question altogether.

So watch today’s press conference for what Powell does and does not say about his own future. Watch the June meeting for the first signal of what the new regime actually looks like. And watch, after that, for whether the Warsh Fed acts like an independent central bank that happens to share some of the President’s preferences, or like a central bank whose preferences are increasingly the President’s by another route.

It is not a rate decision. It is a regime decision.

The chairman leaves today. The hard part starts in June.

Related

Nicole Byers is an entertainment enthusiast! Nicole is an entertainment journalist for the Maple Grove Report.