“If he’s alive or dead it doesn’t matter. If he’s dead, just prop him up and put some dark glasses on him like, like ‘Weekend at Bernie’s.’”

That was John McCain on Alan Greenspan in 2007, about a year and a half after Greenspan had stepped down as chairman of the Federal Reserve. The joke worked because it was almost true. For most of two decades, the markets behaved as though Greenspan’s mere presence was the policy.

Greenspan took over the Fed in 1987 and stood at the helm of the world’s most powerful central bank for nearly twenty years. He became the symbol of American economic primacy, and on the trading floors he was treated as a rock star – bigger than any other economist or policymaker in the 1990s and the early 2000s.

I have often been critical of Greenspan’s economic thinking. But the death of a man who shaped the world economy for a generation is a moment for fairness, and in his case the fair assessment is far more interesting than either the hagiography or the easy dismissal.

The Man Who Made Low Inflation the Fed’s Job

Greenspan cemented two things we now take for granted. The first is central bank independence. The second is that securing low and stable inflation is the Fed’s responsibility, and nobody else’s.

That was not obvious when he arrived. Arthur Burns, who ran the Fed in the 1970s, believed inflation was a cost-push problem of union power and a permissive welfare state, to be managed through “incomes policies” – direct government meddling in private price-setting. Greenspan rejected all of it.

Inflation is always and everywhere a monetary phenomenon. Greenspan ran the Fed as if he believed exactly that, even while he refused to say so plainly.

And he refused to say almost anything plainly. “Since I’ve become a central banker, I’ve learned to mumble with great incoherence,” he told a Congressional subcommittee in 1987. “If I seem unduly clear to you, you must have misunderstood what I said.” It became the most quoted thing he ever said, and it was a tell – the cryptic surface concealed a very clear underlying rule.

Leaning Against the Wind, with Credibility

The rule has a name, and the name comes from my old friend Bob Hetzel, the one of the most respected monetary economists the Federal Reserve ever produced, and a man who wrote his Chicago thesis under Milton Friedman.

Hetzel’s history of the Fed divides the postwar period into competing versions of a single procedure that William McChesney Martin invented in the 1950s and called “leaning against the wind” – raising the policy rate when the economy runs hot, cutting it when the economy weakens.

There are two ways to run it. Under Martin and later Burns, the Fed practised what Hetzel calls leaning against the wind with trade-offs. It waited for inflation to appear in the data, treated low unemployment and low inflation as competing objectives, and tried to buy one with the other. It failed. The 1970s were the bill.

Volcker and Greenspan ran the other version – leaning against the wind with credibility. The Fed moved the funds rate preemptively, before inflation showed up, and in doing so it handed the price system back the job of setting employment and output. Hetzel dates this regime from 1979 to 2006, and it produced the Great Moderation.

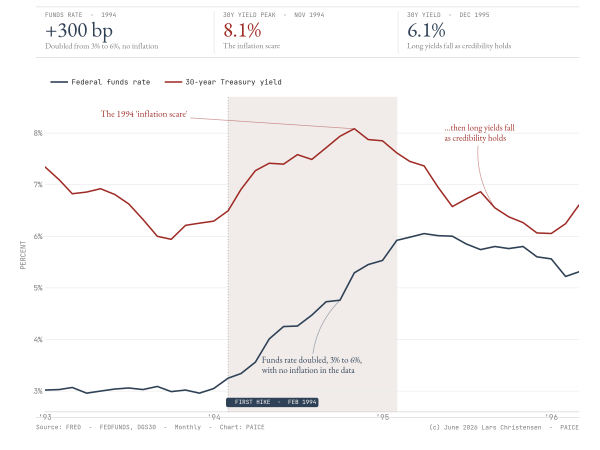

The defining moment was 1994. Greenspan raised the funds rate sharply with no inflation visible in the data, purely to convince the bond market that he meant it. The “inflation scare” passed, and the Fed’s credibility was secured. That, after all, is what credibility buys you: the freedom to act on a forecast rather than wait for a fact.

Take a look at what actually happened.

The funds rate doubled, from 3% to 6%, across 1994. The 30-year yield jumped first – the inflation scare – peaking above 8% as the bond market challenged the Fed. And then it fell back below 6%, even as the funds rate stayed high. The market tested Greenspan, lost, and capitulated. Long yields fall when the market believes you, not when you stop tightening.

This is, in my view, Greenspan’s real achievement, and it is the one most of his admirers misread. It was not his opacity. It was not his famous “feel” for the data. It was a rule – preemptive, forward-looking, and disciplined by the bond market – and he had the discipline, for a while, to follow it.

Greenspan Understood Nominal GDP Better Than He Let On

Here is the part almost nobody remembers. I dug it out years ago and wrote about it on this blog in 2013.

At an FOMC meeting in November 1992, Greenspan told his colleagues that the old monetarist philosophy would have required 4.5% money growth to drive nominal GDP at 4.5%, but that he was “basically arguing” the Fed was using a nominal GDP goal directly, with the money-supply relationships as mere technical mechanisms. And he added that you would know the markets were convinced about price stability when the 30-year Treasury sat near 5.5%.

Read that again. Greenspan was describing nominal GDP targeting, by name, in 1992 – two decades before a small group of economists – including myself – took it up as a cause.

We – what later became known as the Market Monetarists – never claimed it was new. That was the whole point. Nominal GDP stability was what had produced the Great Moderation in the first place, and our argument was simply that making it the Fed’s explicit, rule-bound mandate was the way to restore that stability after it was lost in 2008. Greenspan had been running, by instinct, the thing we wanted written into law.

Through the Great Moderation nominal GDP grew at about 5.5% a year. Potential real output grew at roughly 3%. The 30-year Treasury yield sat near 5%. Inflation ran close to 2.5%.

That is what price stability looks like when it sits on top of a fast-growing supply side. The numbers moved together, year after year, for the better part of two decades.

The chart above makes the point. Actual nominal GDP tracked a steady 5.5% growth path for the better part of two decades. That 5.5% line was never an announced target – it was a de facto one. And sitting on top of roughly 3% real growth, it delivered exactly the low, stable inflation Greenspan is remembered for.

Five and a Half Then, Four Now

The number that secured price stability in Greenspan’s era will not secure it today. And that is not a change of doctrine. It is the same arithmetic applied to a slower economy.

Nominal GDP growth minus trend real growth is, roughly, inflation. In the Greenspan years the sum was about 5.5% nominal, 3% real, and 2.5% inflation. The Fed could run nominal demand at 5.5% and still deliver price stability, because the supply side was growing at 3%.

That extra point of real growth is gone. The Congressional Budget Office now puts US potential growth a little above 2%, drifting toward 1.8% by the 2030s. Run nominal GDP at 5.5% against that, and you do not get 2.5% inflation. You get something closer to 3.5%.

So the right anchor today is lower – nearer 4% nominal GDP growth than 5.5%. In my view a 4% path against roughly 2% trend real growth delivers the same 2% inflation Greenspan delivered. The target moves because the economy underneath it moved.

This is what the nostalgia for Greenspan misses. He was not more relaxed about inflation than a central banker should be now. He simply had 3% real growth to work with, and his successors have barely 2%. The discipline is worth copying. The number is not.

Where the Market Knew Better

But Greenspan trusted his own judgement more than he trusted the market, and that is where it went wrong.

In a post – There never was a bond market “conundrum” – some years ago (2012) I ran a simple thought experiment. A nominal-GDP-targeting Greenspan in 2005 would have said something like this: we have raised rates 150bp, inflation expectations are well contained, long yields are near 4%, and since we are targeting a 5% path for nominal GDP, there is a real chance we have overdone the tightening.

That is not what he said. The real Greenspan questioned the market’s judgement. He was more optimistic about future nominal GDP growth than the bond market was – and the bond market, it turned out, was quietly forecasting a sharp slowdown. The market was the better forecaster. Greenspan was not.

This is the recurring weakness of even the best discretionary central banker. The rule works precisely because it constrains the judgement of the person running it. Greenspan followed the rule when it agreed with his instincts and overrode it when it did not.

The Crisis Came After He Left

Greenspan is usually blamed for 2008. The standard charge is that easy policy in the early 2000s pumped up house prices and equity prices, and that the resulting imbalances blew up in the crisis. I agree with this – partly. Only partly.

I have never believed that a central bank can reliably spot an asset bubble in real time, still less that it should set the policy rate to deflate one. That is not what monetary policy is for. The Fed has one nominal anchor to manage, not a portfolio of asset prices to police.

And here is the detail the bubble story ignores. Greenspan left the Fed at the start of 2006. The catastrophic error of 2008 – keeping policy far too tight relative to the natural rate of interest while nominal GDP was collapsing – happened on someone else’s watch.

Hetzel’s verdict on the Great Recession is that it was monetary disorder, not market failure. The Fed fell back into its old ways in 2007 and 2008, too focused on headline inflation, too slow to see that the natural rate of interest had gone deeply negative. The Great Moderation did not die of natural causes. The Fed killed it.

So the honest charge against Greenspan is narrower than the popular one. He did not cause 2008. But he let the discipline of the rule slip in his final years, and his successors finished the job.

And this points to the failure that is genuinely his. Greenspan ran a nominal GDP rule, but he never wrote it down. He kept it as instinct, as judgement, as the Maestro’s feel for the data – and instinct does not survive the man who has it. Had he turned his de facto target into a transparent, explicit rule that his successors were bound to follow, 2008 need not have happened. The rule was sound. What was missing was the constitution that would have outlived him.

It Happened Again

We know the cost of leaving the rule unwritten, because the Fed paid it twice.

From 2010 to 2019 the Fed ran another de facto nominal GDP rule – a 4% path. I have argued for years that this is what the data show: from 2009 onwards, US nominal GDP behaved as though the Fed had a 4% level target, tracking it almost perfectly, quarter after quarter, just as Greenspan’s Fed had tracked 5.5%. And just as before, it was never written down. It was the practice of a particular set of people, not a commitment the institution was bound to.

So when COVID came and with that massive fiscal and monetary expansion, there was nothing to anchor to.

Nominal GDP did not return to the 4% path once the shock passed. It exploded – growing at about 10.5% a year across 2021 and 2022, a one-off step up in the price level that the Fed never reversed. That was the inflation of 2021-22. And it was not bad luck. It was the predictable cost of running a good rule informally.

An explicit 4% nominal GDP level target would have caught it. The rule would have told the Fed, in early 2021, that nominal demand was running far above the path and had to be pulled back – and it would have acted before inflation became entrenched, not eighteen months too late. The catastrophe could have been avoided, or at the very least made far smaller.

Two regimes, three decades apart. The same de facto rule, the same success while it held, and the same failure the moment discretion took over. That is the case against the Maestro model in a sentence.

A Quieter Achievement: Ending the Draft

There is one part of Greenspan’s career that has nothing to do with monetary policy, and it may be the part that did the most direct good.

In 1969 President Nixon convened the Gates Commission to study whether the United States could end military conscription. Greenspan served on it alongside Milton Friedman, W. Allen Wallis, William Meckling, and Walter Oi – a remarkable concentration of free-market economic talent. They were the intellectual core that made the case for an all-volunteer force.

The argument was elegant, and it was Greenspan’s kind of argument. The draft, the economists showed, was not free. It was a hidden tax levied on the young – the gap between what a conscript was paid and what he would have had to be offered to serve willingly. A volunteer army, properly paid, was not only more just. It was more efficient, because it let the price system do what conscription did by coercion.

In February 1970 the commission recommended, unanimously, that the draft be abolished. The economists won the argument. Conscription ended in the United States in 1973, and more than fifty years later the all-volunteer force is so settled that few Americans remember it was ever in doubt.

Consider what that meant. Generations of young Americans were spared being compelled into uniform against their will, on the strength of an economic argument that Greenspan helped make. He spent most of his life as the most powerful central banker in the world. But on the Gates Commission he was something rarer – one of a handful of economists who used the discipline to expand human freedom directly. That, too, is the Friedmanite in him: the conviction that the price system allocates better, and more humanely, than the state’s compulsion.

The Rule and the Man

No one is going to prop Greenspan up, fit him with dark glasses, and install him back at the Fed. But the thing worth keeping is not the man. It is the rule he ran.

A central bank does not need a Maestro. It needs a rule that is preemptive, predictable, and credible – and the discipline to follow it. Greenspan had the rule, and for most of two decades he had the discipline too. That is no small thing to leave behind.

A central bank does not need a Maestro. It needs a rule – transparent, explicit, and binding on whoever holds the chair next. We have now watched the same lesson twice: a good rule, run on instinct, that worked until the instinct left the room. In 2008, and again in 2021, the cost of never writing it down came due.

So here is the fair verdict. The lesson of Greenspan’s career is not that we should hope for another like him. It is that we should never have to. Build the rule well enough, and the Maestro becomes unnecessary. He will be remembered as the Maestro. He deserves, just as much, to be remembered for the rule he ran – and to stand as the warning about the rule he never quite dared to write down.

Related

Nicole Byers is an entertainment enthusiast! Nicole is an entertainment journalist for the Maple Grove Report.